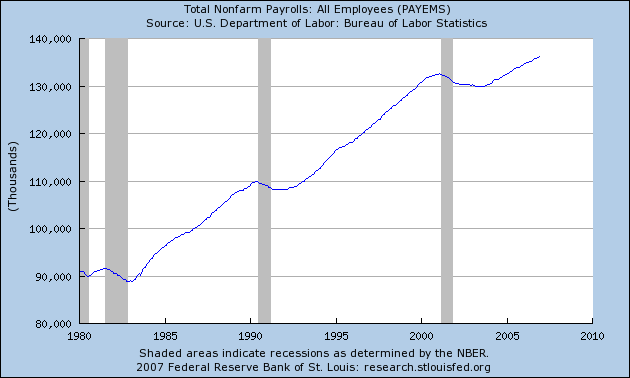

Here is a chart of total establishment jobs.

Notice that establishment jobs continue to increase until right each recession began. This indicates that monthly increases are not necessarily predictive of a continued expansion; job increases can occur right up until the beginning of a recession.

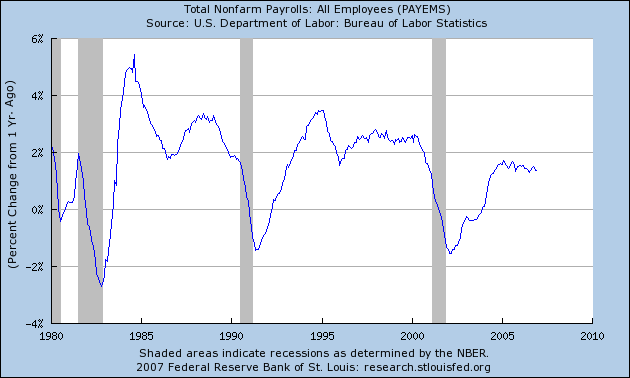

Here is a chart of year-over-year percent change:

This chart gives us something more to work with. Notice how the YOY percent change dropped noticeably before the beginning of the last two recessions. Also note we haven't had a drop of similar magnitude during this expansion. That adds some strength to the soft-landing pundit's arguments.

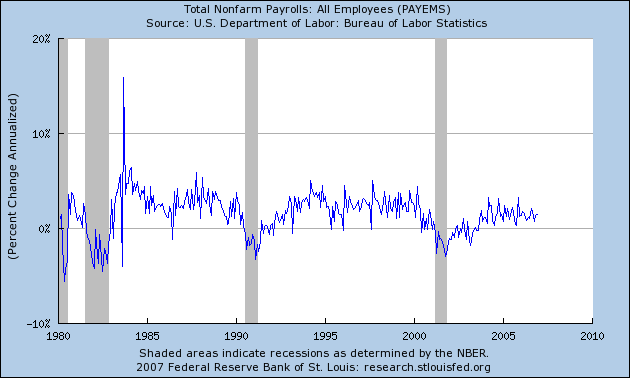

Here is a chart of the percent change annualized rate of change:

This chart has a lot of statistical noise, so it is not as solid as a predictor. However, notice that before the last two recessions, the annualized percent change hit 0%. But also notice that several times the line hit 0% and the economy didn't hit a recession. That makes this particular economic number pretty soft.

So, what do we know now that we didn't know when we started? That year-over-year percent change in establishment payrolls is probably the best employment predictor of recessions; it has dropped sharply before two of the last three recessions. In addition, this chart was last updated on January 5 when the 167,000 payrolls number came out. That means according to this statistic we aren't near a recession yet.

It's important to remember that hiring is an incredibly important business decision -- perhaps one of the most important decisions a business makes. That makes these numbers very important.

It's also important to remember there is no economic holy grail.