Go and do something else aside from economics and market watching.

I'll be back tomorrow afternoon.

Saturday, March 10, 2007

Friday, March 9, 2007

The Markets Today

SPY: -.01%

QQQQ: +.05%

IWN: +.48%

Translation: money flowed into the small cap market today. Everybody else was scratching their heads.

Looking at the charts, we have a lot of meandering in the SPYs and QQQQs. They opened higher, dropped, moved around, sold-off then rallied. The IWNs at least closed higher.

QQQQ: +.05%

IWN: +.48%

Translation: money flowed into the small cap market today. Everybody else was scratching their heads.

Looking at the charts, we have a lot of meandering in the SPYs and QQQQs. They opened higher, dropped, moved around, sold-off then rallied. The IWNs at least closed higher.

Payrolls + 97,000

First a disclaimer. The BLS has revised this number a great deal. Recently they reported they added an additional 800,000 jobs to the 2006 totals. Clearly their current model is pretty flawed.

In today's report we learn the BLS found an additional 35,000 jobs in January with their upward revision for the month.

Be that as it may....

Here's a link to the report.

Construction lost 62,000. The housing slowdown is starting to hit employment numbers. I would expect this number to continually worsen over the next year as the housing slowdown starts to bleed into the rest of the economy.

Here's how the BLS reported it:

The rest of the gains were split between professional, business and leisure jobs.

While total private hourly earnings increased 6 cents, hours worked decreased by .1%. Decreased hours usually makes increased wages a wash.

The last few employment reports have all showed a slowing economy -- even with the subsequent revisions. This report clearly falls within that as well. In addition, we're seeing housing really hit employment. Earlier this month housing starts dropped 16%. That means housing related employment will one decrease further.

Here's a chart from CBS Marketwatch of the last year of job growth:

In today's report we learn the BLS found an additional 35,000 jobs in January with their upward revision for the month.

Be that as it may....

Here's a link to the report.

Construction lost 62,000. The housing slowdown is starting to hit employment numbers. I would expect this number to continually worsen over the next year as the housing slowdown starts to bleed into the rest of the economy.

Here's how the BLS reported it:

In the goods-producing sector, construction employment fell by 62,000 in February after posting a gain of 28,000 in January. Unusually severe winter weather conditions in some areas of the country in February likely contributed to job losses in the industry. Employment declined in both residential (-21,000) and nonresidential (-25,000) specialty trades, and heavy construction lost 10,000 jobs. Employment in residential specialty trades has been declining since February 2006.

Manufacturing employment continued to trend down over the month (-14,000). Job losses occurred in wood products (-4,000), semiconductors and electronic components (-3,000), and textile mills (-3,000). Machinery added 5,000 jobs in February. In mining, employment rose by 4,000.

The rest of the gains were split between professional, business and leisure jobs.

While total private hourly earnings increased 6 cents, hours worked decreased by .1%. Decreased hours usually makes increased wages a wash.

In the service-providing sector, health care employment rose by 33,000 in February, as job growth continued throughout the component industries. Over the year, health care employment has increased by 340,000.

Employment in professional and business services continued to trend up in February (+29,000) with small gains occurring in most of its component industries. Over the past 12 months, this industry has added 460,000 jobs. In February, employment in services to buildings and dwellings grew by 11,000. Temporary help services employment was little changed over the month and over the year.

Elsewhere in the service-providing sector, food services and drinking places added 21,000 jobs in February. Over the year, food services employment has risen by 348,000. Employment in the information industry was up by 13,000 in February. Within financial activities, depository credit intermediation added 4,000 jobs. Over the month, employment was essentially unchanged in both wholesale and retail trade. Air transportation lost 7,000 jobs.

The last few employment reports have all showed a slowing economy -- even with the subsequent revisions. This report clearly falls within that as well. In addition, we're seeing housing really hit employment. Earlier this month housing starts dropped 16%. That means housing related employment will one decrease further.

Here's a chart from CBS Marketwatch of the last year of job growth:

New Century Financial Stops Making Loans

From the WSJ:

I doubt this will be the last we will hear of New Century Financial or the subprime market.

In the clearest sign yet of how rapidly funding is vanishing for the risky loans that helped fuel the housing boom, nervous creditors forced New Century Financial Corp., the nation's second-largest subprime mortgage lender, to stop making new loans.

The Irvine, Calif., company, which has been plagued by rising defaults on its subprime mortgage loans -- home loans made to borrowers with weak credit -- said it has been in talks with its creditors to "identify ways to address their concerns" and obtain more funds in the near term. But it added that "there can be no assurance that these efforts will succeed."

Yesterday, people close to the matter said New Century got fresh financing from one of its biggest creditors, investment bank Morgan Stanley. Even so, the company's mounting woes intensified speculation that it may be forced to file for protection from creditors under Chapter 11 of the federal Bankruptcy Code unless it can find a suitor or sell assets soon.

I doubt this will be the last we will hear of New Century Financial or the subprime market.

Subprime Problems May Increase Housing Inventory

From Bloomberg:

Existing housing inventory is one of the reasons I have been bearish on the housing market.

Housing inventory is expressed as "months available for sale given current sales rates." Another way to put this is "how many months would it take to clear existing inventory at current sales rates?" According to the Census Bureau there are currently enough new homes on the market for 6.8 months of sales at the current sales rate. This number has jumped around between 5.2 and 6.8 for the last year. Eyeballing the numbers, it looks like the lower 6s is about the median.

According to the National Association of Realtors there were 3.549 million existing homes on the market in January or 6.6 months of inventory. An increase of 500,000 would increase that level to a little over 4 million. Those totals won't come onto the market all at once. Instead, they will come onto the market gradually, which will make clearing existing inventory that much more difficult.

Rising mortgage defaults by subprime borrowers may add more than 500,000 homes to a residential real estate market already beset by slumping prices, according to CreditSights Inc.

In January, 4.09 million new and existing homes were offered for sale, down from 4.43 million in July 2006, the National Association of Realtors and the U.S. Commerce Department said. New homes accounted for 536,000 of the January total, down from a record 573,000 in July.

A five-year housing boom that ended a year ago was fueled in part by the growth of mortgage products marketed to borrowers with poor credit histories. Now, as defaults on subprime loans surge to a seven-year high, more than 20 lenders have closed or sought buyers since the start of 2006. The survivors are raising their lending standards.

``We estimate that the effect of looser lending standards could translate into another 533,000 homes coming onto the market as borrowers default -- an unwelcome phenomenon given the existing supply surplus,'' Sarah Rowin and Frank Lee of bond research firm CreditSights wrote in a March 1 report.

Existing housing inventory is one of the reasons I have been bearish on the housing market.

Housing inventory is expressed as "months available for sale given current sales rates." Another way to put this is "how many months would it take to clear existing inventory at current sales rates?" According to the Census Bureau there are currently enough new homes on the market for 6.8 months of sales at the current sales rate. This number has jumped around between 5.2 and 6.8 for the last year. Eyeballing the numbers, it looks like the lower 6s is about the median.

According to the National Association of Realtors there were 3.549 million existing homes on the market in January or 6.6 months of inventory. An increase of 500,000 would increase that level to a little over 4 million. Those totals won't come onto the market all at once. Instead, they will come onto the market gradually, which will make clearing existing inventory that much more difficult.

More on Retail Sales

This is a graph from Investors Business Daily

Note that sales are still growing, but they are coming in below where analysts thought they were.

Here's the salient points from IBD:

Also, read The Big Pictures hilarious take on the recent news in retail sales.

Note that sales are still growing, but they are coming in below where analysts thought they were.

Here's the salient points from IBD:

February's soft showing came in the wake of solid January sales gains, lifted by a late month cold snap. As a result, retailers entered February with much of their winter goods cleared — and well stocked for spring.

But when the cold hit, shoppers didn't want spring apparel and couldn't find coats or sweaters.

"In February the last thing you wanted to buy was a spring outfit," Perkins said. "And if you were going to buy for now there wasn't much in the stores."

The month's adverse weather held down February same-store sales by at least half a percentage point, said Michael Niemira, chief economist at the International Council of Shopping Centers.

Because February typically has the year's second lowest sales volume behind January, one shouldn't extrapolate too much from the month's results, he said.

Also, read The Big Pictures hilarious take on the recent news in retail sales.

Thursday, March 8, 2007

Daily Market Charts

Because the employment report is so important right now, I think it's a good idea to get a look at the daily market charts before the news release. I think they all say pretty much the same thing, so here they are in the following order: SPYs, QQQQs IWNs

We had the big down day, followed be a slightly less pronounced decline. All three charts have a classic candlestick hammer style bottom. While we had a relief rally over the last few sessions, notice it's been on declining volume. In addition, the candle bars of the rally are weak -- the open and closes are very close. All of these factors can signal the rally is losing steam and traders are looking for a reason to sell. In addition, all three averages are approaching their respective 10-day moving averages, which could be a resistance line for all three.

Again, this is not set in stone. We're simply trying to play the averages about what could happen.

We had the big down day, followed be a slightly less pronounced decline. All three charts have a classic candlestick hammer style bottom. While we had a relief rally over the last few sessions, notice it's been on declining volume. In addition, the candle bars of the rally are weak -- the open and closes are very close. All of these factors can signal the rally is losing steam and traders are looking for a reason to sell. In addition, all three averages are approaching their respective 10-day moving averages, which could be a resistance line for all three.

Again, this is not set in stone. We're simply trying to play the averages about what could happen.

The Markets Today

The closing price indicates this was a good day -- the SPYs were up .76%, the QQQQs were up .91% and the IWNs were up 1.03%. But we had two big sell-offs -- one during the last half hour of trading. Traders are obviously nervous about tomorrows employment report.

In addition, note how the markets spiked up at the beginning, but couldn't hold onto these gains throughout the day. This further indicates nervousness.

In addition, note how the markets spiked up at the beginning, but couldn't hold onto these gains throughout the day. This further indicates nervousness.

Housing and Employment

Big thanks to Bonddad's girlfriend for this from MSNBC:

I looked at housing and employment about 6 months ago. A conservative reading of job growth puts housing related jobs at about 30% of total growth for this expansion. That's including construction, financial and professional services. In other words, housing is really important to this expansion.

The blog Calculated Risk has estimated that between 200,000 to 400,000 jobs will be lost as housing cools. Additionally, we really haven't started to see the big drop because housing starts are just starting to slow. Business construction may absorb some of these losses, but as of now we don't know how many.

Now the housing slump is hitting yet another target: housing-related jobs, a list that includes everyone from the people who build and sell houses to makers of appliances and furnishings.

That's a sharp contrast to the height of the housing boom in 2005-06, when the industry was responsible for creating some 25,000 to 50,000 new jobs every month, according to Mark Zandi, chief economist at Moodys.com.

“In the recent months it’s been laying off workers at a pace of 25,000 to 50,000 per month,” he said. “And I think the next couple of quarters we’ll start seeing job losses of between 50,000 and 75,000 per month. ... I think the housing market is going down a whole other notch.”

I looked at housing and employment about 6 months ago. A conservative reading of job growth puts housing related jobs at about 30% of total growth for this expansion. That's including construction, financial and professional services. In other words, housing is really important to this expansion.

The blog Calculated Risk has estimated that between 200,000 to 400,000 jobs will be lost as housing cools. Additionally, we really haven't started to see the big drop because housing starts are just starting to slow. Business construction may absorb some of these losses, but as of now we don't know how many.

Retail Sales Disappoint

From Bloomberg:

This is another piece of bad economic news this week. We had a drop in durable goods and productivity and higher labor costs. The Beige Book was slightly optimistic, but noted it had concerns with housing. It also said nothing had change on the inflation front, implying rates aren't coming down anytime soon.

While this report isn't horrible because sales are still positive, its weakness may imply the consumer is slowing down his retail purchases.

The coldest February since 1979 caused U.S. retailers' sales to grow at the slowest pace in 11 months as consumers delayed purchases of spring merchandise.

Wal-Mart Stores Inc., the world's biggest retailer, said sales at stores open at least 12 months rose 0.9 percent, less than the company's forecast of 1 percent to 2 percent. Luxury stores and retailers with designer clothes, including Target Corp., the second-largest U.S. discount chain, fared better, with sales surpassing analysts' estimates.

Total U.S. same-store sales rose 2.4 percent, the smallest gain since March 2006, the International Council of Shopping Centers said based on results from 51 retailers. The majority of retailers missed estimates after cold weather cut demand for shorts, dresses and spring merchandise, while a snowy Valentine's Day in the U.S. Northeast kept some shoppers home.

``We hate to hear weather as an excuse, but I think it was pretty legitimate this month,'' said Lori Wachs, who helps manage $100 billion at Philadelphia-based Delaware Investments, including retail shares. Retailers ``are going to have a lot of ground to make up in March.''

This is another piece of bad economic news this week. We had a drop in durable goods and productivity and higher labor costs. The Beige Book was slightly optimistic, but noted it had concerns with housing. It also said nothing had change on the inflation front, implying rates aren't coming down anytime soon.

While this report isn't horrible because sales are still positive, its weakness may imply the consumer is slowing down his retail purchases.

Memo to Employers: Lose the Second Yacht

| |

| Why is Pace University making it so hard for Chris Williams to get a union contract? |

On March 1, the House voted 241–185 for the Employee Free Choice Act, which would establish stronger penalties for violation of employee rights when workers seek to form a union and during first-contract negotiations. It also would allow employees to form unions through a majority verification process, in which workers sign cards to indicate their support for a union.

In attacking the bill, Big Business has misleadingly insisted it would take away the secret ballot election process by which workers now form unions. But that argument is a red herring. First of all, Employee Free Choice Act doesn’t take away the secret ballot process. Workers will have a choice between the ballot process and majority verification.

Second, as currently run by the nation’s labor board, this management-controlled election process is anything but democratic. The long, drawn-out process gives management plenty of time to harass and intimidate workers—and let’s face it, how many people want to join a union if their employer threatens to fire them (which 25 percent of private-sector employers do, even though it is illegal)?

Former Labor Secretary Robert Reich puts it this way:

A secret ballot sounds democratic, but workplaces aren’t democracies because employers have the power to hire and fire. That's where the potential for intimidation lies. And the only way around it is to go with a simple up-or-down vote.There are many examples of how the so-called “election process” doesn’t work. Chris Williams, an adjunct physics professor at Pace University in New Jersey, shared his story with us at the AFL-CIO. In December 2003, Williams and a majority of his co-workers signed authorization cards saying they wanted to be represented by New York State United Teachers/AFT (NYSUT/AFT). Pace University's administration then went to enormous lengths to block them from winning recognition and a contract. (A majority of workers can sign authorization cards now—but employers are not required to recognize the union. The Employee Free Choice Act would fix that.) Why would Williams, a well-educated professional, want to join a union? Says Williams:

I would starve to death if I had to rely on my wages from Pace. I'd be homeless. The average pay for an adjunct for a three-credit course is just $2,500 for a 15-week course.While a tenured professor might earn $100,000 per year, an adjunct faculty member in the next classroom with the same qualifications would earn subsistence pay of only $15,000 for the equivalent of a full-time workload. (What was that again from the Bush administration about lack of education behind the nation’s low-wage economy? We’ll address that canard in a future post.)

The adjunct faculty then tried the election process route of the National Labor Relations Board (NLRB). First, the university tried to delay the election. Then, after the election was held in spring 2004 and the adjunct faculty voted overwhelmingly for the union, the university came up with a bizarre legal argument that hundreds of adjunct faculty members should be excluded from the bargaining unit. It actually refused to include them in negotiations with the union. The director of NLRB's Region 2 found the disputed adjunct faculty members were part of the bargaining unit, and the five-member NLRB in Washington, D.C., rejected a request by the university to have the region's decision overturned. But even now, Pace is appealing the decision to the federal appeals court. That postpones the adjunct faculty's rights even longer. So a staggering two-and-a-half years of negotiations have passed and the adjunct faculty still has no contract.

That's why Williams, who sees firsthand the flaws in the current system, supports the Employee Free Choice Act, which provides for mediation and then arbitration if managements and unions can't work out a contract in 90 days.

So, given that most businesses are not interested in running their workplaces like a democracy (“How many people want a four-week vacation? Raise your hands”), we thinketh they doth protest too much that the bill would take away this nonexistent freedom.

Business interests also say workers would be “coerced” into joining a union through the majority verification process. That presumes most workers don’t want to join a union. That presumption is wrong. In fact, some 60 million U.S. workers say they would join a union if they could, based on research conducted by Peter D. Hart Research Associates in December 2006.

Commenting on the American Chronicle, Stephen Crockett, co-host of Democratic Talk Radio, points out how employer cries of intimidation are directed in the wrong direction.

The intimidation is almost entirely on the side of the companies. Companies are in a position of power over workers. Co-workers are simply not in a similar power situation. Only the company is really in the kind of power position to intimidate workers.Most critically, the bill is about economic justice: Full-time workers in unions had median weekly earnings of $833 in 2006, compared with $642 for their nonunion counterparts, and are far more likely to have good health and retirement security. In March 2006, 80 percent of union workers in the private sector had jobs with employer-provided health insurance, compared with only 49 percent of nonunion workers. Union workers also are more likely to have retirement and short-term disability benefits.

And its here—in the dollars and cents—we find the real reason for employer opposition to the Employee Free Choice Act. The past two decades have seen an unprecedented growth in compensation only for top executives and a dramatic increase in the ratio between the compensation of executives and their employees. The average CEO made 411 times the salary of the average worker in 2005. That’s up from 42 times in 1980—a tenfold increase. Meanwhile, average worker's pay increased to about $43,000 in 2004 from about $36,000 in 1980, an 0.8 percent a year increase—about 19 percent total increase—in inflation-adjusted terms.

The average CEO of a Standard & Poor's 500 company made $13.51 million in total compensation in 2005, according to an analysis by The Corporate Library. And that's just the annual take. Seems like what CEOs really fear about the Employee Free Choice Act is that by granting their workers family-supporting wages and health care and retirement security, they might have to forgo that second yacht.

Again, Robert Reich:

America's rising economic tide has been lifting executive yachts, but leaving most working people in leaky boats. Workers need more bargaining power. They should be allowed to form a union when a majority of them wants one. As simple as that.

Beige Book is Out

The Federal Reserve Issued the Beige Book yesterday. Here's a link to the report.

Here are some highlights from various news sources:

WSJ:

From CBS Marketwatch:

From Bloomberg:

From Reuters:

I would encourage everybody to read the full report and all of the news articles as they provide some of the best insight into what the Federal Reserve policy makers are thinking.

Here are some highlights from various news sources:

WSJ:

The report found "modest expansion in economic activity" in many districts, including the regions centered on Chicago, Minneapolis and Philadelphia. But some districts noted some slowing, including Dallas, Boston and St. Louis. It also noted continued demand for skilled workers and some pressure to increase wages

From CBS Marketwatch:

Housing markets remained weak, although there were "signs of stabilization" in some areas.

Manufacturing activity was "steady or expanding," despite the weakness in auto- and housing-related production.

Retail sales were said to be growing steadily. Auto sales were sluggish.

Inflation was "little changed." Pay increases were "moderate."

From Bloomberg:

The general tone of the report was upbeat, describing continued growth in retail sales, services and demand for labor. Policy makers are alert for signs of a deeper economic slowdown after last week's global equities rout and reports showing a prolonged decline in housing.

``I still think that the underlying economic fundamentals are conducive to a pickup in growth as we move through 2007 and 2008,'' Chicago Fed President Michael Moskow said today in a speech in Chicago. ``I am not prepared to significantly change my projections.''

From Reuters:

Policy-makers expect the economy to slowly pick up after losing steam in the fourth quarter as housing cooled. The Beige Book nodded to hopes that this sector might finally be on the mend, while softness among manufacturers remained confined to autos and products linked to residential construction.

I would encourage everybody to read the full report and all of the news articles as they provide some of the best insight into what the Federal Reserve policy makers are thinking.

Hedge Funds and Sub-Prime Lenders

From the WSJ:

Live by the subprime, die by the subprime.

Seriously, this highlights an interesting and perhaps difficult problem in the market. Hedge funds don't make any disclosure reports to the SEC. Therefore, we don't know what they are investing in. We also don't know how many hedge funds are investing in the subprime mortgage area or in what concentration.

This means there could be a few more hedge funds out there reeling from the subprime shakeout. This could lead to a wave of redemptions and a ton of problems in the market.

Hedge-fund investors betting on the riskiest home-mortgage loans are learning a difficult lesson: The higher they fly, the further they fall.

Consider the volatility at Second Curve Capital -- a hedge-fund firm run by Thomas Brown, a former Wall Street research analyst -- which recently has been hammered betting on the stocks of "subprime" lenders, which cater to high-risk borrowers.

The two main funds at Second Curve were down 8% and 10% in January -- and at least as much last month. Hedge-fund databases show the funds' losses for February at 12.5% and 14%, though Mr. Brown contends that the performance was comparable to January.

In any case, it is a significant turnabout from 2006, when the Second Curve funds rose nearly 55%. In 2005, Mr. Brown's funds were down 2%, after soaring 60% in 2004. With $600 million under management, Mr. Brown tends to invest in highly concentrated areas of the financial world, accentuating the bumps.

Live by the subprime, die by the subprime.

Seriously, this highlights an interesting and perhaps difficult problem in the market. Hedge funds don't make any disclosure reports to the SEC. Therefore, we don't know what they are investing in. We also don't know how many hedge funds are investing in the subprime mortgage area or in what concentration.

This means there could be a few more hedge funds out there reeling from the subprime shakeout. This could lead to a wave of redemptions and a ton of problems in the market.

Wednesday, March 7, 2007

DR Horton: "2007 Is Going to Suck"

From CNN:

Pretty hard to misinterpret that comment.

"I don't think '08 is going to be a great year, but it's going to be much better than '07," CEO Don Tomnitz told the Citigroup Industrial Manufacturing Conference

He also said: "'07 is going to suck."

D.R. Horton said it may have to make further write-offs to reflect unsold homes or lower land values.

"We may have more impairments coming," Tomnitz said. "We'll know that on a quarter-by-quarter basis."

Pretty hard to misinterpret that comment.

Markets Drop at Close

I've been posting the daily stock charts since the market sold-off last week. After a big sell-off, the daily charts can give us an idea of what traders are thinking about the market and let us know about the overall confidence level in the market.

Today we had a big sell-off in the SPYs and QQQQs at the end of the trading day. This indicates that traders don't want to hold positions overnight. This indicates a lack of confidence -- or at least a return of caution.

Today we had a big sell-off in the SPYs and QQQQs at the end of the trading day. This indicates that traders don't want to hold positions overnight. This indicates a lack of confidence -- or at least a return of caution.

Oil Inventories Drop; Gas Prices Increase

From CBS Marketwatch:

Looking at the charts from This Week In Petroleum, we see that gas inventories have been dropping for the last few weeks while the oil inventory just dropped this week.

Here's another chart of interest -- gas prices:

They've been ticking up lately.

Crude-oil futures climbed Wednesday to touch a high of $62 a barrel after U.S. data showed that supplies of crude declined for the first time in three weeks and distillate and gasoline inventories have been falling for several weeks.

"Import dynamics caused surprises in inventory changes," said Jason Schenker, an economist at Wachovia Corp.

"Lower crude and gasoline imports engendered a surprise draw in crude inventories and a larger-than-expected gasoline draw," he said an in e-mailed note to clients. And "the distillate inventory draw was mitigated by increased imports."

Crude for April delivery was last up $1.16 at $61.85 a barrel on the New York Mercantile Exchange, following a climb to as high as $62.

Looking at the charts from This Week In Petroleum, we see that gas inventories have been dropping for the last few weeks while the oil inventory just dropped this week.

Here's another chart of interest -- gas prices:

They've been ticking up lately.

Great New Webpage

I've always like Briefing.com. The link just listed is to a new page that keeps a running tab on up/down volume etc... by the hour. It's a really good page and I'm surprised it took somebody this long to do this.

Homebuilders See Tough Year

From Bloomberg:

We're seeing some very large drops -- 20%+ and 1000 less homes indicates demand is waning. In addition, we still have a ton of inventory on the market at current demand levels that will take awhile to work off.

I thought housing was going to lead the US into recession by the current quarter. However, as the industry still languishes I think the blog Calculated Risk had it right: we're going to see lots of little cuts emerge in the US economy over the coming months. Expect to see declining construction employment, lower mortgage equity withdrawal numbers and lower home construction impacting overall GDP growth.

So far housing's problems have remained in the housing market. Only time will tell if that lasts.

A year after the housing slump began, the spring selling season is off to a rocky start with a glut of unsold properties and buyers like the Binghams putting off purchases, thwarting any chance of a recovery. The National Association of Home Builders in Washington now expects sales to fall for the sixth consecutive quarter after last month predicting a gain. The biggest stock market rout in four years last week, a jump in subprime mortgage failures and concerns about a possible recession are keeping consumers on edge.

....

Builders are bracing for another tough year after seeing 2006 sales plunge 17 percent, the most since 1990. For some, such as Toll Brothers Inc., the largest U.S. builder of luxury homes, the lackluster spring market is a surprise. Chairman and Chief Executive Officer Robert Toll told investors three months ago the market may be poised to rebound. It didn't happen.

``We're all a little more disappointed than we were two weeks ago,'' Toll said Feb. 22 on a conference call, responding to questions about February sales. ``We didn't have anywhere near the bump up that we usually see.''

The same day, Horsham, Pennsylvania-based Toll Brothers cut the number of homes it expects to build to 6,000 to 7,000, the second reduction in four months. In August, the company's estimate was 7,000 to 8,000 homes. Toll Brothers also lowered its fiscal year profit outlook on Feb. 22.

Miami-based Lennar Corp., the biggest U.S. builder by revenue, expects new home deliveries to tumble 20 percent this year. Hovnanian Enterprises Inc. of Red Bank, New Jersey, the industry's sixth-largest company, reported a fiscal first-quarter loss after the number of contracts signed slid 23 percent.

We're seeing some very large drops -- 20%+ and 1000 less homes indicates demand is waning. In addition, we still have a ton of inventory on the market at current demand levels that will take awhile to work off.

I thought housing was going to lead the US into recession by the current quarter. However, as the industry still languishes I think the blog Calculated Risk had it right: we're going to see lots of little cuts emerge in the US economy over the coming months. Expect to see declining construction employment, lower mortgage equity withdrawal numbers and lower home construction impacting overall GDP growth.

So far housing's problems have remained in the housing market. Only time will tell if that lasts.

Oil Market Update

The following paragraph about the oil market caught my eye:

Here's the daily chart of oil:

Notice that despite the sell-off this week, the market is still in an uptrend. Because we're close to the current trend-line, this week's action is pretty important from a technical perspective.

However, there are strong fundamental reasons for oil to increase. Once again, remember that we have India and China growing. So long as these economies are making large GDP advances there will be upward pressure on commodity prices. We're also entering the summer driving season in the US, adding further upward pressure.

"There is an expectation that when the equity markets complete the current correction, oil will resume its upward trajectory to test the 65 usd level," noted Harris.

Here's the daily chart of oil:

Notice that despite the sell-off this week, the market is still in an uptrend. Because we're close to the current trend-line, this week's action is pretty important from a technical perspective.

However, there are strong fundamental reasons for oil to increase. Once again, remember that we have India and China growing. So long as these economies are making large GDP advances there will be upward pressure on commodity prices. We're also entering the summer driving season in the US, adding further upward pressure.

Mortgage Risk Premiums Increasing

From the WSJ:

Mortgages are eventually pooled with other mortgages of similar maturity and interest rate and sold to investors. This process is done for all mortgage products. The commercial mortgage backed market is usually considered more secure because businesses are considered more stable than households.

If this market is seeing an increase in its risk premium, other markets must be. That means the cost of issuing and packaging mortgages has gotten more expensive.

Turmoil in the market for bonds backed by home mortgages is starting to infect its commercial cousins: mortgage bonds backed by office towers, hotels and shopping malls.

The cost of insuring commercial-mortgage-backed securities as measured by an index known as the CMBX has jumped since late last month. The spread on the index that tracks riskier, BBB-minus-rated bonds has doubled to 1.64 percentage points this week from 0.84 percentage point on Feb 23, according to Markit Group, which administers the index.

"Moves of this magnitude and speed are uncommon in the unusually calm CMBS markets," noted analysts from Lehman Brothers in a report this week.

Mortgages are eventually pooled with other mortgages of similar maturity and interest rate and sold to investors. This process is done for all mortgage products. The commercial mortgage backed market is usually considered more secure because businesses are considered more stable than households.

If this market is seeing an increase in its risk premium, other markets must be. That means the cost of issuing and packaging mortgages has gotten more expensive.

Tuesday, March 6, 2007

Court Dates Tomorrow

In my real life (not my super-secret econo-geek super-hero life) I'm a trial lawyer. I'll be in court for most of tomorrow.

I'll be up early to check the headlines for what's interesting, but probably won't be back online until mid-afternoon CST (I live in Houston). Hopefully I'll be back in time for the market close to see how the markets perform.

BD

I'll be up early to check the headlines for what's interesting, but probably won't be back online until mid-afternoon CST (I live in Houston). Hopefully I'll be back in time for the market close to see how the markets perform.

BD

Markets Bounce Back

It looks like the bleeding has stopped -- at least for now. The markets rallied today. The SPYs were up 1.79%, the QQQQs were up 1.71% and the IWNs were up 2.74%. Below are the charts in the previously mentioned order. Notice the markets rallied well all day. They sold off a touch at the end, but that is to be expected. What's important going forward is traders are willing to hold their positions overnight.

I should add, this sure feels like a dead-cat bounce to me. The news today was uniformly bad -- productivity was down, new orders dropped and employment costs rose. This means

1.) Businesses will have a harder time passing on increased input prices.

2.) The economy is slowing, and

3.) Inflationary pressures may be increasing, or at the least holding steady.

All three together are very bearish news, adding further evidence that today's rally was mostly technical in nature.

I should add, this sure feels like a dead-cat bounce to me. The news today was uniformly bad -- productivity was down, new orders dropped and employment costs rose. This means

1.) Businesses will have a harder time passing on increased input prices.

2.) The economy is slowing, and

3.) Inflationary pressures may be increasing, or at the least holding steady.

All three together are very bearish news, adding further evidence that today's rally was mostly technical in nature.

Productivity Down, Labor Costs Up

From CBS Marketwatch:

From Bloomberg:

This is terrible news -- on a terrible news day.

There has been a fair amount of speculation about when the Fed would lower rates. This news hems the Fed in a heck of a lot more. Lower productivity means businesses are less able to absorb inflationary pressures (rising input prices). That means they will pass increasing costs onto consumers.

The higher labor costs -- even if it is a one time affair -- add to inflationary pressures as well. The one-time factor may help to limit this effect, but the number will still probably get some notice.

The U.S. economy appears less productive and more inflation-prone than suspected.

Productivity of the U.S. nonfarm business sector rose at a 1.6% annual rate in the fourth quarter, weaker than the 3.0% pace estimated a month ago. Read full government report.

Unit labor costs -- a gauge of wage push inflationary pressures - were revised higher to a 6.6% annualized gain from a 1.7% increase. Unit labor costs are the costs paid to workers to produce one "unit" of output. This is the largest quarterly gain since the first three months of 2006.

Unit labor costs have increased 3.2% in the past year, the fastest pace since 2000.

From Bloomberg:

U.S. workers were less productive last quarter than initially estimated and labor costs jumped, making it harder for the Federal Reserve to reduce interest rates even as manufacturing and housing continue to slump.

Productivity, a measure of how much an employee produces for each hour of work, rose at an annual rate of 1.6 percent, down from the 3 percent pace reported last month, the Labor Department said today in Washington. Labor costs climbed 6.6 percent, reflecting a one-time increase in bonuses. Separately, the Commerce Department said factory orders fell in January by the most in more than six years.

The figures mean inflation may be slow to dissipate even though economic growth is tailing off, creating headaches for Fed Chairman Ben S. Bernanke as concerns about a possible 2007 recession mount. Housing, whose slump triggered the slowdown in growth, so far shows few signs of bouncing back: A report from the National Association of Realtors today showed fewer Americans signing contracts to buy previously owned homes.

This is terrible news -- on a terrible news day.

There has been a fair amount of speculation about when the Fed would lower rates. This news hems the Fed in a heck of a lot more. Lower productivity means businesses are less able to absorb inflationary pressures (rising input prices). That means they will pass increasing costs onto consumers.

The higher labor costs -- even if it is a one time affair -- add to inflationary pressures as well. The one-time factor may help to limit this effect, but the number will still probably get some notice.

Factory Orders Drop Big

From the Census Bureau

Let's break this number down.

The following numbers are the seasonally-adjusted numbers.

The overall new orders number was down 7.8%. ButBoeing transportation orders can make this number incredibly noisy. However, even without transportation orders, this number was still down 3.1%.

The 9.6% drop in unfilled manufacturing orders indicates back-orders are getting cleared out. That makes the drop in new orders that much more important as it appears manufacturers are clearing out their old orders and will have fewer orders going forward.

There was a 9.3% drop in new machinery orders and a 7.8% drop in new computer and electronic products orders. This means that capital spending plans may be dropping in the business sector.

Here's how Bloomberg reported the number:

New orders for manufactured goods in January, down following two consecutive monthly increases, decreased $22.9 billion or 5.6 percent to $383.1 billion, the U.S. Census Bureau reported today. This followed a 2.6 percent December increase.

Shipments, down following three consecutive monthly increases, decreased $4.6 billion or 1.2 percent to $391.2 billion. This followed a 1.3 percent December increase.

Unfilled orders, up twenty of the last twenty-one months, increased $0.6 billion or 0.1 percent to $695.2 billion. This was at the highest level since the series was first stated on a NAICS basis in 1992 and followed a 2.3 percent December increase. The unfilled orders-to-shipments ratio was 4.78, up from 4.71 in December. Inventories, down following ten consecutive monthly increases, decreased $0.9 billion or 0.2 percent to $482.0 billion. This followed a 0.2 percent December increase. The inventories-to-shipments ratio was 1.23, up from 1.22 in December.

Let's break this number down.

The following numbers are the seasonally-adjusted numbers.

The overall new orders number was down 7.8%. But

The 9.6% drop in unfilled manufacturing orders indicates back-orders are getting cleared out. That makes the drop in new orders that much more important as it appears manufacturers are clearing out their old orders and will have fewer orders going forward.

There was a 9.3% drop in new machinery orders and a 7.8% drop in new computer and electronic products orders. This means that capital spending plans may be dropping in the business sector.

Here's how Bloomberg reported the number:

Orders placed with U.S. factories declined by the most in more than six years in January on lower demand for aircraft, computers and construction machinery.

Factory orders fell 5.6 percent after a 2.6 percent increase in December that was larger than previously reported, the Commerce Department said today in Washington. Excluding transportation equipment such as Boeing Co. jets, bookings fell 2.9 percent, the biggest decline since September.

Business spending on new equipment fell by the most in more than five years as declines in the auto and construction industries took a toll on manufacturing. Weaker corporate investment, together with continued efforts to reduce bloated stockpiles, are likely to be a drag on growth this quarter, economists said.

``Manufacturing had a tough January as the inventory adjustment grinds on,'' said Joshua Shapiro, chief U.S. economist at Maria Fiorini Ramirez Inc. in New York. ``Capital spending is off to a weak start in the first quarter.''

GM -- $1 Billion in Bad Mortgages

From Bloomberg:

Continuing...

The sub-prime story is beginning to filter into the broader market. I seriously doubt this will be the last event in this area.

General Motors Corp., the world's largest automaker, may take a charge of almost $1 billion to cover bad mortgage loans made by its former home-lending unit, according to a Lehman Brothers Holdings Inc. analyst.

Residential Capital LLC relies on loans to people with poor or limited credit records or high debt burdens, for more than three-quarters, or $57 billion, of its loan portfolio, Lehman analyst Brian Johnson wrote in a research report. Delinquency rates on such subprime loans made last year are at a record high.

Continuing...

About 13 percent of the subprime loans backing bonds issued in 2006 and rated by S&P are delinquent, with 6.65 percent of the loans behind in payments by 90 days or more, according to Standard & Poor's. More than 20 lenders have closed or are seeking buyers since the beginning of 2006. Subprime mortgages typically have rates at least two or three percentage points above safer prime loans.

``Some traders are expressing their view that we're a pure mortgage market play, whether that's appropriate or not,'' Louise Herrle, ResCap's treasurer, said in an interview last week.

The sub-prime story is beginning to filter into the broader market. I seriously doubt this will be the last event in this area.

Commodoties Take Hit

From the Financial Times:

Over the last month or so I have written a few articles about a possible summer rally in commodities. See here and here. Both of these articles relied on technical analysis.

It's easy to sell TA as a "holy grail" of investing. This is the way it was sold when I first started reading about it in the late 1980s/early 1990s. However, I would strongly encourage readers to look at the writings of Gann, Gartley and Schabacker. All three wrote in the 1930s era and all of their writing provides the baisc underpinnings of modern TA theory.

All three also make the following paraphrased observation: the markets will make an ass of you whenever and wherever they can. And they are very good at making an ass of you, so don't get cocky.

This week's market action clearly highlights technical analysis' shortcomings. By relying solely on chart patterns without any fundamental knowledge of the markets a trader can get killed.

I think the following paragraph from the above article still makes sense:

India and China are still growing. That's a little under 2 billion people who are living in economies growing at 8% or more. They want stuff. As I wrote in one of the articles:

Fundamental analysis tells you what to buy.

TA tells you when to buy.

I will caution: it can all change tomorrow.

The recent volatility in global financial markets hit the commodities sector hard on Monday, as hedge funds and other investors scurried to reduce their risky investments.

Nickel prices tumbled 5 per cent, while copper and zinc fell almost 3 per cent and gold prices traded at levels more than 7 per cent lower than before the start of last week’s market turmoil.

This repositioning is prompting some unusual price swings and heavy trading flows, particularly in sectors that have been the focus of risk-taking over the past year, such as credit derivatives, emerging markets and commodities.

“I don’t think anything has fundamentally changed for commodity markets. I think it is just a case of investors selling their holdings to pay for losses they may have incurred elsewhere,” said Kevin Norrish, commodities analyst at Barclays Capital.

An adviser to a London-based fund of hedge funds added: “The big theme of the moment is deleveraging and derisking.”

Over the last month or so I have written a few articles about a possible summer rally in commodities. See here and here. Both of these articles relied on technical analysis.

It's easy to sell TA as a "holy grail" of investing. This is the way it was sold when I first started reading about it in the late 1980s/early 1990s. However, I would strongly encourage readers to look at the writings of Gann, Gartley and Schabacker. All three wrote in the 1930s era and all of their writing provides the baisc underpinnings of modern TA theory.

All three also make the following paraphrased observation: the markets will make an ass of you whenever and wherever they can. And they are very good at making an ass of you, so don't get cocky.

This week's market action clearly highlights technical analysis' shortcomings. By relying solely on chart patterns without any fundamental knowledge of the markets a trader can get killed.

I think the following paragraph from the above article still makes sense:

“I don’t think anything has fundamentally changed for commodity markets. I think it is just a case of investors selling their holdings to pay for losses they may have incurred elsewhere,” said Kevin Norrish, commodities analyst at Barclays Capital.

India and China are still growing. That's a little under 2 billion people who are living in economies growing at 8% or more. They want stuff. As I wrote in one of the articles:

Remember we still have China and India on-line for very strong growth rates, increasing demand for base metals.

Fundamental analysis tells you what to buy.

TA tells you when to buy.

I will caution: it can all change tomorrow.

Subprime Problems In Graph Form

This chart is from the WSJ:

Notice a few things.

1.) Defaults now are higher than they were in 2002-2003 at the beginning of this expansion.

3.) '02-'03 were the first two full years of this expansion.

That means sub-prime mortgage delinquencies are higher now -- 6 years into the expansion -- than they were at the beginning of the expansion.

A simple explanation may be delinquency rates were coming down in 20-03. This is possible. However, the fact we are six years into an expansion and delinquency rates are this high may indicate other problems -- such as the effect of lending money to everybody who has a pulse.

Notice a few things.

1.) Defaults now are higher than they were in 2002-2003 at the beginning of this expansion.

3.) '02-'03 were the first two full years of this expansion.

That means sub-prime mortgage delinquencies are higher now -- 6 years into the expansion -- than they were at the beginning of the expansion.

A simple explanation may be delinquency rates were coming down in 20-03. This is possible. However, the fact we are six years into an expansion and delinquency rates are this high may indicate other problems -- such as the effect of lending money to everybody who has a pulse.

Monday, March 5, 2007

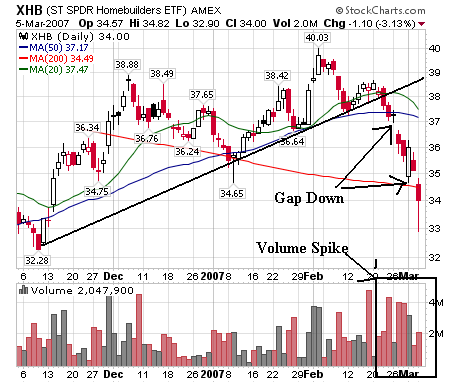

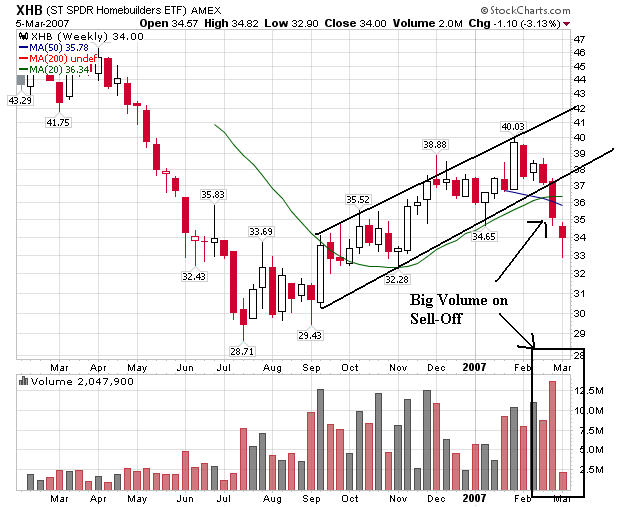

Homebuilders Rally Looks Over

The homebuilders stocks enjoyed a rebound that traced back to the beginning of the recent stock rally. However, that rally looks over at this point.

Here's the daily chart

Notice we have two gaps down with a large volume on the sell-off.

Here's the weekly chart:

This chart more clearly shows the drop-off that's occurred. Notice the uptrend is clearly broken.

Here's the daily chart

Notice we have two gaps down with a large volume on the sell-off.

Here's the weekly chart:

This chart more clearly shows the drop-off that's occurred. Notice the uptrend is clearly broken.

Sub Prime Blues Continue

From Yahoo News:

The use of the phrase "cease and desist" sounds like some type of illegal event was happening. In reality, this is the FDIC saying, "you need to stop doing business in this manner."

Fremont General Corp. intends to exit its sub-prime residential real estate lending operations, the company said Friday.

The move was prompted by a Proposed Cease and Desist Order Fremont General received from the Federal Deposit Insurance Corp. on Feb. 27 that calls for the company to make a variety of changes to restrict the level of lending in its sub-prime residential mortgage business, among other things.

The use of the phrase "cease and desist" sounds like some type of illegal event was happening. In reality, this is the FDIC saying, "you need to stop doing business in this manner."

Markets Drop; Charts Look Terrible

The markets are closed. The SPYs lost .9% the QQQQs lost .97% and the IWNs lost 2.12%. Clearly people are getting out of small caps.

With the charts below, notice

1.) All the markets had a downward bias

2.) Traders dumped stock at the end of the day, indicating a lack of confidence about the overnight situation

3.) The increased volume at the end of the day.

With the charts below, notice

1.) All the markets had a downward bias

2.) Traders dumped stock at the end of the day, indicating a lack of confidence about the overnight situation

3.) The increased volume at the end of the day.

ISM Decreases But Still Expansive

From the ISM:

Overall business activity decreased, but any reading above 50 is considered a sign of expansion.

New orders and the backlog of orders decreased slightly, but far from an alarming rate. The decrease could be accounted for as pure statistical noise.

New export orders increased faster than new import orders. While the US still has an incredibly long way to go until it deals with the trade imbalance, any possible sign of improvement is a good thing.

"Non-manufacturing business activity increased for the 47th consecutive month in February," Nieves said. He added, "Business Activity and New Orders increased at a slower rate in February than in January. Employment increased at a faster rate than in January. The Prices Index decreased 1.4 percentage points this month to 53.8 percent. Nine non-manufacturing industries reported increased activity in February. Members' comments in February are mixed concerning current business conditions. The overall indication in February is continued economic growth in the non-manufacturing sector, but at a slower pace than in January."

Overall business activity decreased, but any reading above 50 is considered a sign of expansion.

New orders and the backlog of orders decreased slightly, but far from an alarming rate. The decrease could be accounted for as pure statistical noise.

New export orders increased faster than new import orders. While the US still has an incredibly long way to go until it deals with the trade imbalance, any possible sign of improvement is a good thing.

Markets Open Lower

As of this writing, the markets gapped down on the open.

Hang on -- it's going to be another bumpy week.

Hang on -- it's going to be another bumpy week.

Gas and the S&P

This chart is from TickerSense -- one of my favorite econ/market blogs. Notice the inverse relationship between gas prices and the S&P 500 for the last year or so.

How Fast Will the Carry Trade Go Away?

From Seeking Alpha:

The difference between Japanese and US interest rates is still large -- to the tune of 500+ basis points. However, even the hint of the carry trade (borrowing in Japan and lending in the US) going away has serious implications for the US and Japanese markets.

Japan's Ministry of Finance reports Q4 (ended Dec.) capital spending increased 16.8%, beating the prior quarter's reading of 12.0% and analysts' estimates of 13.0% to 14.2% (Reuters). Up to a 1.0% revision to Q4 GDP is expected. Jesper Koll, chief economist at Merrill Lynch Japan, says annualized Q4 GDP will be revised to 5.1% from 4.8%, adding that "It is a trigger point for the Bank of Japan to normalize interest rates a little more aggressively." Bloomberg quotes Koll who also says, "The crisis of the 1990s is definitely over. Japan is in the process of building a strong platform for very strong, competitive economic growth." An economist at Nikko Citigroup however, says a revised GDP is not necessarily good due to concerns over rising inventories which "may prompt adjustments in production in coming months." The yen rose 1.7% today to ¥115.6/$1 as of the market's close in Tokyo. Japanese stocks meanwhile fell for a fifth straight day, as the Nikkei 225 lost 3.3% to 16,642.

The difference between Japanese and US interest rates is still large -- to the tune of 500+ basis points. However, even the hint of the carry trade (borrowing in Japan and lending in the US) going away has serious implications for the US and Japanese markets.

Asian and European Stocks Tank

From the WSJ:

The rest of the region and Europe was just as ugly.

It's going to be a bumpy week.

Asian stocks dropped sharply across the region, with Japanese shares declining for the fifth session in a row, while Hong Kong retreated 4%.

Japan's Nikkei 225 Index fell 3.34% to 16642.25, extending a slide for a fifth day that was sparked by last week's plunge in Chinese and U.S. stock markets. Exporters were hit hardest on the yen's recent rally. Since climbing to its highest in nearly seven years last Monday, the index has slid 1573.10 points, or 8.64%, over the last five trading sessions.

The rest of the region and Europe was just as ugly.

Markets in Hong Kong, Australia, the Philippines, Malaysia, India and South Korea all fell sharply Monday, continuing their declines from last week, when a 9 percent plunge in Chinese stocks on Tuesday triggered cascading selloffs on Wall Street and other global markets.

European markets also opened lower Monday, with Britain's benchmark FTSE 100 down 1.5 percent in early trading, France's CAC 40 sliding 1.8 percent and Germany's DAX sinking 2.1 percent.

It's going to be a bumpy week.

HSBC's Yearly Bad Debt Coverage Increases 36%

From the WSJ:

This isn't going to be the last we hear about this, from HSBC or any other bank that has subprime exposure. This story is going to last awhile.

HSBC Holdings PLC, reporting its 2006 results, said the cost to cover bad debts soared 36% to $10.57 billion in 2006 because of the bank's ill-fated move to buy risky subprime loans from U.S. originators.

Overall, the London bank said net income rose 4.7% to $15.79 billion in 2006 from $15.08 billion. HSBC is the world's third-largest bank ranked by market value behind Citigroup Inc. and Bank of America Corp.

In 2005 and 2006, HSBC's U.S. business, HSBC Finance Corp., increased the number of subprime mortgage loans it bought from originators. But amid increasing interest rates and slowing housing price appreciation, borrowers defaulted at record rates, including in 2006 where loans were just months old. Last month, the bank replaced the top management of its U.S. operations and acknowledged that it had made mistakes in its mortgage strategy.

This isn't going to be the last we hear about this, from HSBC or any other bank that has subprime exposure. This story is going to last awhile.

Sunday, March 4, 2007

The Long-Term Perspective

Here is a 5-year chart of the SPYs, QQQQs and IWNs in a weekly format. Notice three things.

1.) We are still in an uptrend.

2.) Just eyeballing the charts, we would have to move at least 5% more to the downside before we moved into secular bear market territory.

3.) Volume really spiked last week. That could indicate the beginning of at least a short-term correction.

1.) We are still in an uptrend.

2.) Just eyeballing the charts, we would have to move at least 5% more to the downside before we moved into secular bear market territory.

3.) Volume really spiked last week. That could indicate the beginning of at least a short-term correction.

The Week Ahead

We have some important economic news coming out.

Monday we have the non-manufacturing ISM survey. This will give us a gauge of the service economy.

Tuesday we have factory orders, which will further clarify the durable goods number from last week. We also have productivity which will help to provide some guidance on the inflation number.

The Beige Book comes out on Wednesday. This is a great read for eco-nerds.

Friday is the big number: jobs. The economy has slowed for the last three quarters, so this figure will either confirm or deny that figure.

We also have markets in a technically bad place, so we should have a wild ride.

Monday we have the non-manufacturing ISM survey. This will give us a gauge of the service economy.

Tuesday we have factory orders, which will further clarify the durable goods number from last week. We also have productivity which will help to provide some guidance on the inflation number.

The Beige Book comes out on Wednesday. This is a great read for eco-nerds.

Friday is the big number: jobs. The economy has slowed for the last three quarters, so this figure will either confirm or deny that figure.

We also have markets in a technically bad place, so we should have a wild ride.

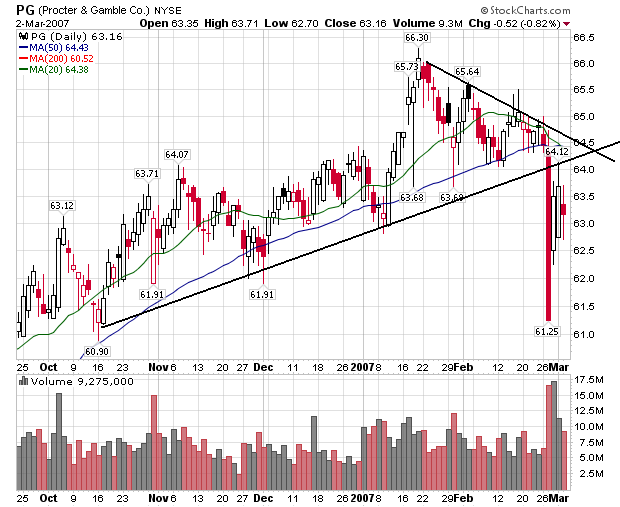

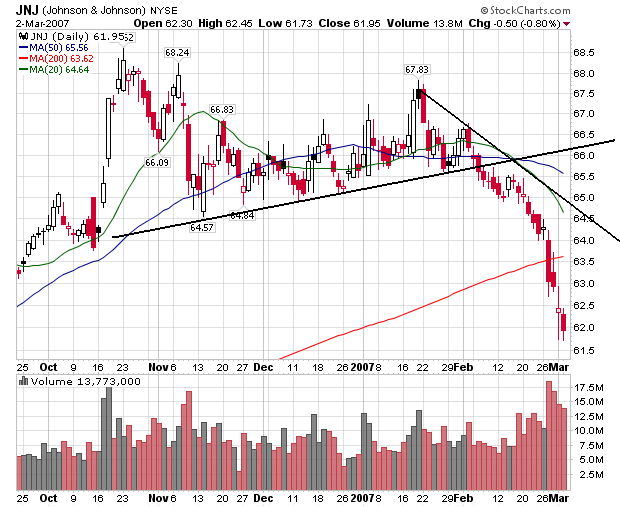

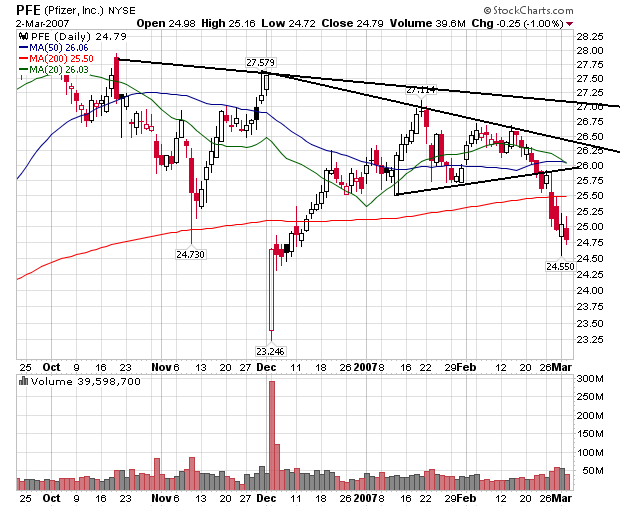

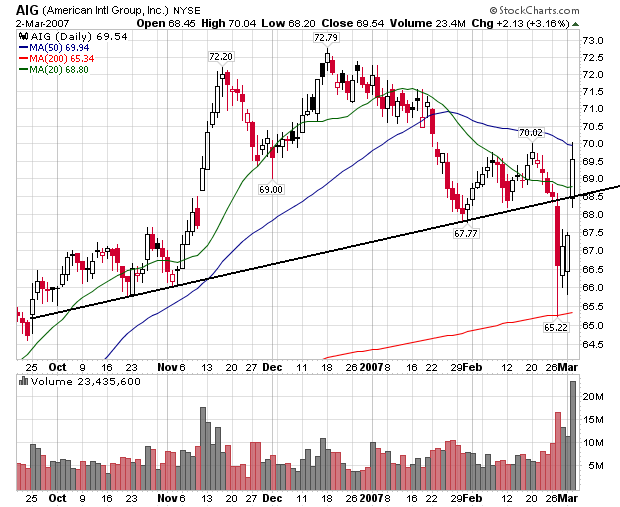

S&P Top 10 Stocks

Here is a list of the second set of top 5 stocks in the S&P 500. Collectively these stocks represent about 7.5% of the overall average. They are listed from the largest to smallest as a percentage of the average.

With the exception of AIG, all of these stocks are in clear downtrends. When you combine these charts with the top 5 S&P stocks you get a pretty dismal picture of the big S&P positions: 8 of the 10 largest caps in the index -- representing about 20% of the average -- are in downtrends. Citigroup is close to a downtrend and the only reason AIG is in an uptrend is an incredibly favorable special circumstance YOY earnings performance (Last year AIG's earnings were low because of a legal settlement).

With the exception of AIG, all of these stocks are in clear downtrends. When you combine these charts with the top 5 S&P stocks you get a pretty dismal picture of the big S&P positions: 8 of the 10 largest caps in the index -- representing about 20% of the average -- are in downtrends. Citigroup is close to a downtrend and the only reason AIG is in an uptrend is an incredibly favorable special circumstance YOY earnings performance (Last year AIG's earnings were low because of a legal settlement).

The Week Ahead: Fundamentals v. Technicals

As I wrote below, the bear case going forward is based on negative fundamentals - subprime housing problems and slower economic growth. In contrast, the the bull case is almost purely technical, essentially arguing the market isn't cheap but not overly expensive right now. Up until now, bullish traders have also had strong technical reasons to stay glued to their charts irrespective of fundamental news. Now those charts are showing bearishness and possible technical reversals. I think it's going to be hard for them to maintain their bullishness going forward. In addition, I think they will pay more attention to bearish news going forward.

Food for thought.

Food for thought.

Feds Issue Dub-Prime Guidance

From Yahoo Financial News:

Not to sound cold-blooded, but the MBA statement sounds like nothing more than a soundbite. 20% of the loans Countrywide services are delinquent; according to UBS 2006 vintage subprime loans are performing poorly right out of the gate.

This isn't about denying credit to worthy borrowers who need a break; it's about not issuing credit simply because someone has a pulse.

In addition, here's some really big news:

Translation: liquidity is drying up -- big time.

Federal bank regulators, worried about a surge in defaults on high-risk home mortgages, called on lenders to exercise caution in making subprime loans and strictly evaluate borrowers' ability to repay them.

The proposed guidance issued Friday by the Federal Reserve and the other four federal agencies that regulate banks, thrifts and credit unions, comes in an increasingly troubled market for subprime mortgage loans. Home-mortgage delinquencies and foreclosures are spiking, especially for people who took out subprime mortgages -- higher-interest loans for those with blemished credit records or low incomes who are considered higher risk -- during the sizzling housing boom that waned in the second half of 2005.

The regulators said the guidelines, if formally adopted by the agencies and followed by lending institutions, could result in fewer borrowers qualifying for subprime loans. The mortgage industry had hoped for less stringent guidelines.

John Robbins, chairman of the Mortgage Bankers Association, said the group was concerned that the guidelines "may restrict credit to many consumers in high-cost areas and deny credit to many deserving low-income, minority and first-time home buyers."

Not to sound cold-blooded, but the MBA statement sounds like nothing more than a soundbite. 20% of the loans Countrywide services are delinquent; according to UBS 2006 vintage subprime loans are performing poorly right out of the gate.

This isn't about denying credit to worthy borrowers who need a break; it's about not issuing credit simply because someone has a pulse.

In addition, here's some really big news:

On Tuesday, Freddie Mac, the nation's second-largest financer of home loans, said it will stop buying those subprime mortgages that it deems most vulnerable to default or foreclosure.

Translation: liquidity is drying up -- big time.

Subscribe to:

Posts (Atom)