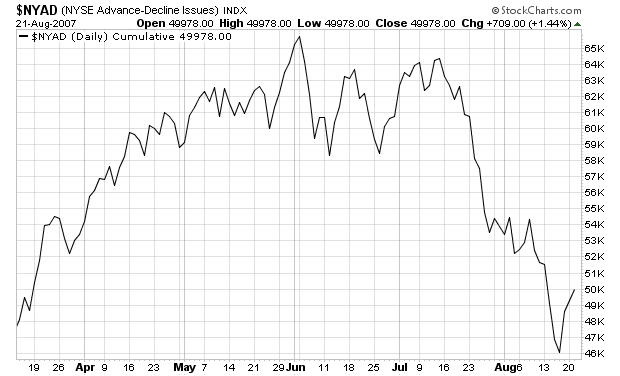

Now, onto the markets. The market has been rallying for the last 6 days and has established two upward trending channels. This is a good sign for the bulls. Here is the 6-day chart which shows the entire pattern.

Here is he daily chart. As I have noted, my primary concern with this chart is the lack of volume. However, that could be explained by simple, post-sell-off concern about the quality of the overall market right now. There are some other very postive signs in this daily chart. Note the 10 and 20 day SMA are now starting to move up. Should the overall market trend continue we will see the 10-day SMA cross the 20 day SMA in the next two weeks or so. If this happens we'll have another bullish signal. Also note that prices are over the 200 day SMA, which is the standard line the separates bull and bear markets.

Here's a 1-year chart of the daily MACD. Notice that it has started moving up again.

Here's the 3-year, weekly chart of the MACD which also shows a possible reversal of the sell-signals from the indicator.

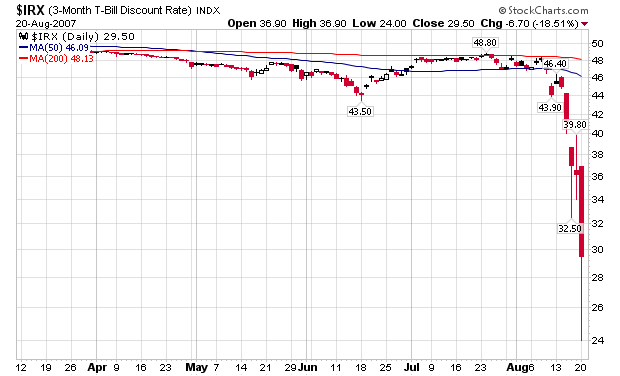

The Fed's lowering of the discount rate is the obvious catalyst for this advance. However, there have also been fundamental reasons for the underlying uptrend. For example, there was no news of any hedge fund blow-ups last week. I have commented before that it will take 2-4 weeks of no news weeks for a solid change to happen in investor psychology. Now we have 1 week.

There have also been signals that the private market is starting to heal itself. For example, Bank of America bought $2 billion of Countrywide preferred stock last week. There was also this news from the New York Federal Reserve:

The Federal Reserve Bank of New York targeted investor gridlock in the asset-backed commercial paper market today, giving banks new information on how they can use such securities as collateral in exchange for central bank loans.

``In response to specific inquiries, the Federal Reserve Bank of New York has affirmed its policy to consider accepting as collateral investment quality asset-backed commercial paper'' for discount-window loans, Andrew Williams, a spokesman for the bank in New York, said in an interview.

The clarification is the latest effort by central bankers to lubricate credit markets, which have shut out some companies after a slide in the value of securities backed by subprime mortgages. The Fed a week ago cut the so-called discount rate on direct loans to banks and encouraged lenders to use the resource. The four largest U.S. banks borrowed $2 billion this week.

In short, there are signs that various actors are starting to make the beginning moves needed to unlock the credit markets.

I want to caution here -- we aren't out of the woods by any stretch of the imagination. There are some serious problems in the financial market right now that aren't going away anytime soon. And we are still a few announcements of big problems away from another sell-off. In other words, if you're going long right now, make sure you have sell stops set.