Let's look at the reasons a currency rallies.

1.) The country's interest rates are increasing. Here is the money quote from the latest Fed statement:

Although downside risks to growth remain, the upside risks to inflation are also of significant concern to the Committee. The Committee will continue to monitor economic and financial developments and will act as needed to promote sustainable economic growth and price stability.

To me, this statement leans towards an increase. But, it doesn't say we're going to increase rates. Instead, it says the "upside risks to inflation are high." But also note the Fed has been saying for some time they expect commodity prices to decrease (which they are right now). So that might take some of the bite out of this statement.

So long as commodity prices continue to decrease or remain where they are for now, there is no reason from a policy perspective (price stability) of increasing rates.

2.) A growing economy. Do I have to lay this done again? The economy is in the early stages of a recession. If you don't see that then you're an idiot.

So -- the two primary fundamental reasons for a currency to increase are gone. That means there is a non-fundamental reason for the dollar's rally.

And indeed there is. There has been a fundamental change in the European interest rate outlook.

The euro fell the most in almost eight years against the dollar as traders pared bets the European Central Bank will raise interest rates as the economy slows.

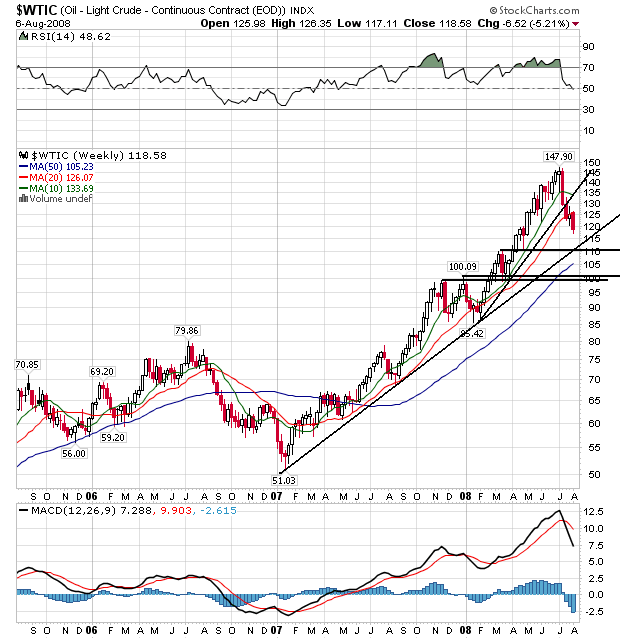

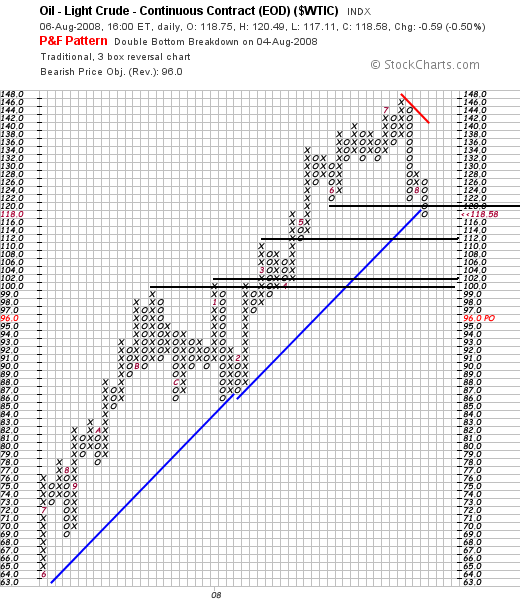

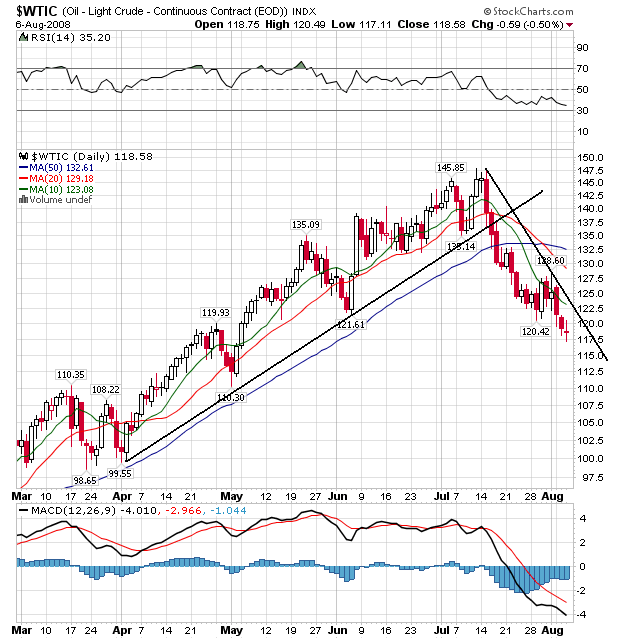

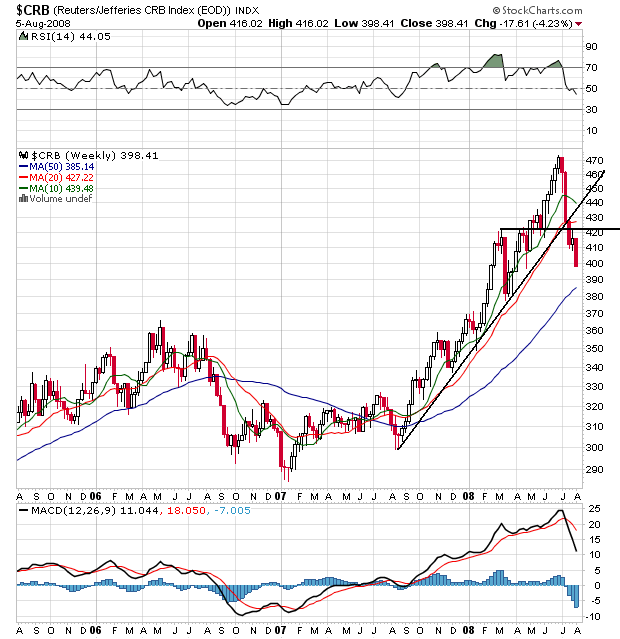

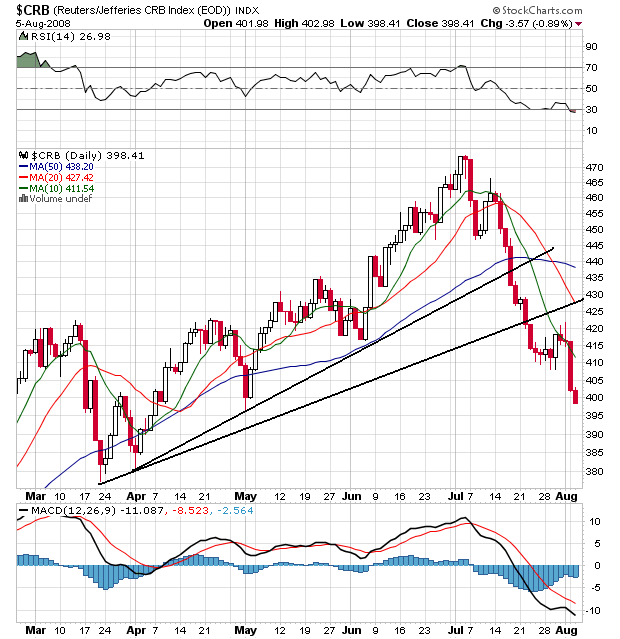

The euro is poised for its biggest weekly loss since January 2005 after ECB President Jean-Claude Trichet yesterday said economic growth will be ``particularly weak'' through the third quarter. An index that tracks the dollar against the currencies of six U.S. trading partners touched the highest since February. Crude oil fell to a three-month low, silver reached its cheapest since January and copper headed for its biggest weekly drop since March, easing inflation concerns.

``This is the beginning of a new chapter for the dollar as Trichet and other central banks are paying more attention to the downside risk to growth,'' said Dustin Reid, a senior currency strategist at ABN Amro Bank NV in Chicago. ``The decline of oil prices is a significant driver behind this dollar rally because it enables other central banks to turn their eyes away from inflation and focus on growth.''

In other words, there is nothing that has changed regarding the US economy or the Federal Reserve. There is a big change in the EU area. That means the dollar isn't increasing but the euro is falling. That's a big difference then a dollar rally.