First, let's look at why economists are talking about a recovery in the first place.

1.) The Philadelphia Fed's manufacturing index has been rising since just after the first of the year,

2.) ...as has New York's Empire State Index.

3.) The Richmond Fed's Manufacturing Index is now in positive territory

4.) ... as is the ISM Manufacturing Index.

5.) Industrial Production appears to have bottomed, printing two consecutive months of increases,

6.) ... along with two months of increases in capacity utilization.

7.) The rate of decline in durable goods orders has bottomed.

So -- we have seven different indicators that say the worst is over for the manufacturing sector. The regional fed surveys and the ISM have all climbed from incredibly low levels to show expansion.

8.) The index of leading economic indicators has increased strongly for the last 5 months.

9.) The threat of deflation -- which was one of the primary reasons for the massive stimulus plan -- is not an issue.

This is extremely important. The threat of deflation was one of the primary reasons for the stimulus spending. Deflation is what led to the great depression. Here's what happens. Consumers stop spending. Retailers lower their prices to attract buyers. This lowers retailers profit margins leading to more lay-offs. Lower sales means lower production of consumer goods which leads to more lay-offs. This lowers consumer demand and the process repeats itself. However, now there is moderate inflation. That indicates that somewhere in the economy there is enough demand pull or cost push from somewhere to increase prices.

10.) The credit markets have stabilized.

11.) The yield curve is showing expansion.

12.) The corporate and junk bond markets have rallied indicating a return of investor's risk appetite.

13.) The housing market appears to have stabilized.

14.) The pace of retail sales bottomed at the beginning of the year

15.) ... as did personal consumption expenditures.

16.) While the pollster.com's average of "is the economy getting better/getting worse" still shows more people thing the economy is getting worse, the percentages have been consistently increasing since March of this year.

17.) Commodity prices have increased (see charts for copper and industrial metals)

18.) Semi-conductor sales have increased for 6 straight months.

19.) Other economies have started to show growth.

20.) Rail traffic has increased on a the month to month basis.

21.) The stock market has rallied about 50%.

22.) The IPO market is starting to thaw.

23.) The M&A market is starting to show some life.

24.) The ISM services index is now positive.

In other words, there are numerous reasons to argue the economy has bottomed and is on the mend. In addition, there are some incredibly healthy developments in the list above. Consider the increase in inflation which indicates that pricing power exists at some point in the economy. Then there is the healing of the credit markets as demonstrated by the a2/p2 spread or the stabilization in both new and existing home sales.

Let's add one important factor to this discussion. Unemployment is a lagging indicator -- in decreases after the economy turns around. In other words, we're not in a position to even consider a decreasing unemployment rate yet.

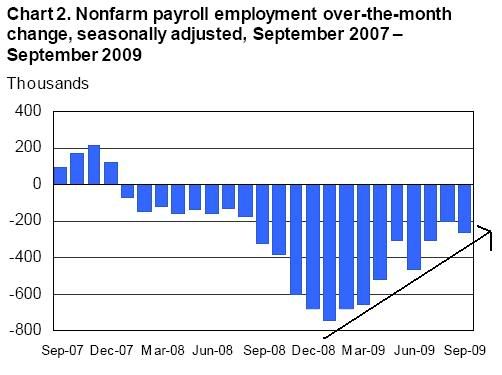

Then there is the jobs situation, which is still the one main sticking point to a full-blown recovery. Let's take a look at the data to see where we are:

The above chart tells us the economy has yet to print a job loss of less than 200,000 -- a troubling sign. However, in the latest employment report, the BLS also told us they revised the total number of jobs lost during the recession lower by an additional 800,000+ thousand. That means that instead of coming down from a period where the economy lost 600,000/month at the end of last year and the beginning of this year, the rate of decline was even sharper. That indicates we're coming up from a deeper hole meaning an even longer recovery period then previously thought. Note that I have continually said about those who are arguing based solely on the jobs issue: an economy that losses over 2 million jobs in 4 months is not going to print a positive employment number anytime within the next 9-12 months." Now we know we are coming from a deeper hole.

My position on the jobs situation relative to the economy has changed to "I have no idea right now." When the jobs report first came out, I was extremely disappointed because the rate of decline failed to drop below 200,000. However, I did not consider completely the balance of information -- that is, considering the amount of news indicating the economy has bottomed verses the jobs situation. The reality is there are numerous data points that indicate we've reached bottom. It's not just one number. Consider: manufacturing is growing, housing sales have bottomed, consumer spending has bottomed, other economies are growing, the credit markets have healed, commodities are rallying, risk appetite has returned, semiconductor sales have increased, rail traffic is increasing. If it were one data point versus the jobs report, it would be a no brainer. But it's not. We have a ton of information pointing to a bottom and nascent recovery. In addition, the downward revision of the total jobs lost for this recession tells us we're digging out from an even deeper hole than before. That logically lengthens the time required to get back to a time of jobs creation. And finally, there is the issue of unemployment which is a lagging indicator. That means we shouldn't even be talking about the drop in the unemployment rate yet.

In short, when I figure it out I will let you know.