We'll be back on Monday. Until then:

The monetary value of all the finished goods and services produced within a country's borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The increase in real GDP in the third quarter primarily reflected positive contributions from personal consumption expenditures (PCE), exports, private inventory investment, federal government spending, and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

Real personal consumption expenditures increased 3.4 percent in the third quarter, in contrast to a decrease of 0.9 percent in the second. Durable goods increased 22.3 percent, in contrast to a decrease of 5.6 percent. The third-quarter increase largely reflected motor vehicle purchases under the Consumer

Assistance to Recycle and Save Act of 2009 (popularly called, “Cash for Clunkers” Program). Nondurable goods increased 2.0 percent in the third quarter, in contrast to a decrease of 1.9 percent in the second. Services increased 1.2 percent, compared with an increase of 0.2 percent

Real nonresidential fixed investment decreased 2.5 percent in the third quarter, compared with a decrease of 9.6 percent in the second. Nonresidential structures decreased 9.0 percent, compared with a decrease of 17.3 percent. Equipment and software increased 1.1 percent, in contrast to a decrease of 4.9 percent. Real residential fixed investment increased 23.4 percent, in contrast to a decrease of 23.3 percent.

Real exports of goods and services increased 14.7 percent in the third quarter, in contrast to a decrease of 4.1 percent in the second. Real imports of goods and services increased 16.4 percent, in contrast to a decrease of 14.7 percent.

-- INVICTUS

Those who have followed anything I’ve written over the years over at Blah3, or more recently here at the Bonddad Blog, know that I have the utmost respect for former Merrill Lynch economist David Rosenberg (now of Toronto’s Gluskin Sheff). I think Rosie’s one of the best in the business, and has always called it as he’s seen it. To his great credit, he was always unwilling to simply toe the sell-side line and blow bullish smoke up everyone’s behind, despite often catching flak for his bearish posture. He was foretelling the story of our recent catastrophe – particularly as it relates to the housing bubble – long before anyone else (including Roubini or Taleb) was onboard. And, unlike them, he was very specific about what was going to trigger the recession -- he wrote about a housing market bubble forming in August 2004 and articulated very clearly that trouble was brewing as a result of it.

When Rosie left Merrill, there was almost immediately a very subtle, very nuanced shift toward a more bullish posture. And when the announcement was made that Ethan Harris was to replace him, the bullish spin went into overdrive (how could it be otherwise when you’ve now got an economist forecasting 3%+ GDP growth for the next six quarters?).

Lately, it seems as though the rhetoric has been escalating.

Those who have followed Rosie know two things for sure about his work, since he hammered them home every chance he could (almost daily):

1) The U.S. consumer – whose Debt-to-Income ratio rose to the stratosphere in an orgy of consumption – needs to return to a more frugal existence, spending less and saving more. As I detailed recently, a mere return to the long-term trendline of Debt-to-Income implies a shedding of about $1.6 trillion of debt (reversion to the mean implies a shedding of over $5 trillion).

2) Rosie has maintained – and continues to do so – that this will be the mother of all jobless recoveries (it arguably already is given the how far we are from the recession’s starting point and the fact that we’re still bleeding jobs).

Now, Rosie’s taken his shots – broadly speaking – at economists who never saw the recession coming and are now opining about a V-shaped recovery. And he’s referred to them in not-so-glowing terms (e.g. shills, hacks, montebanks, etc.), although he’s rarely mentioned anyone by name (though once in a while he lets one fly). In all fairness, it must be pointed out that Rosie has remained steadfastly bearish in the face of the stock market’s 60% rally, and legitimate criticism could certainly be leveled against him on that front.

Now it appears Merrill has decided to retaliate against what they must perceive as Rosie’s assault against their change in perspective since his departure.

In an Oct. 9 piece that purports to refute Rosie’s view of the consumer -- A balanced view of household rebalancing – the Merrill team argues that the U.S. consumer is in better shape than folks like Rosie think, and adds this zinger for good measure: “However, our results strongly contradict some of the more alarmist views on the consumer.” It continues: “The popular press suggests an extreme deleveraging by U.S. consumers is likely. We think this view is unlikely, as households can restore their net worth in several ways. Households could choose either to pay down debt or to accumulate assets, in

order to restore their net worth.”

Their upshot: “None of this should take away from the bottom line: the extreme deleveraging predictions discussed elsewhere need not occur if households actually care much more about their net worth rather than just their debt ratio. Under what we believe are a reasonable set of assumptions, the household sector can repair its balance sheet by pushing up the saving rate to anywhere from 5 to 10%. This should restrain the growth in consumer spending in the coming years, but only by about ¼ to ¾% per year.”

The gist of the argument is that households are more focused in net worth than on debt or on debt-to-income and that, in any event, they could restore the balance by “accumulating assets in order to restore net worth.” How they could accumulate those assets in the absence of either higher incomes, lower debt, or increased savings remains unexplained. (Last I checked, assets had to be paid for somehow, or am I mistaken about that?)

In another shot across the bow (Oct. 20), they take aim squarely at the “jobless recovery” that most (led by Rosie) are forecasting:

Reasons this recovery can be particularly jobless

Turn to page A3 of today's Wall Street Journal, "Employers Hold Off on Hiring". Even though the profit outlook is improving, many companies are holding off on hiring. The WSJ points out that the situation is so bleak in the labor market that even if the economy was churning out jobs as quickly as the 1990s expansion (2.2 million private sector jobs a year), it would still take the economy until 2017 to reach a 5% unemployment rate. While hiring usually lags the economic recovery, the WSJ highlights several reasons why the outlook may be worse this time around:

1 Many businesses have doubts about the durability of the upturn and attribute much of the recent growth in orders to government stimulus and a temporary inventory rebuild.

2 Businesses face uncertainty over the regulatory outlook and the costs associated with the expansion of health care and climate legislation.

3 Companies have also been able successful at boosting productivity to make up for the sharp declines in headcount.

4 Many companies also have excess labor on hand - after cutting hours to record lows, companies can boost production simply by increasing hours without having to add existing workers.

Reasons we disagree with the jobless recovery view

Of course, the first two factors have some merit at the margin but are unlikely to be major drivers of hiring activity, in our view. The productivity argument arises after each recession and works for a time until the typical lag we normally witness in the relationship between activity and hiring kicks in. The final point is the one that is, in our view, most mistaken. Although it is true that hours have been cut to record lows, that does not mean there is excess labor. Not all labor is fungible and there could be demographic and work rule reasons why firms have chosen to cut hours rather than production in certain industries. Finally, a number of industries work with such a lean workforce that, when the downturn came, these workers saw their hours cut as the alternative was for the plant to shut down - these industries were not likely going to be the drivers of growth in the labor market under any circumstances.

I don’t find either of their arguments particularly compelling.

Yesterday, as a matter of fact, the Merrill team had to contend with what can only be described as a huge setback in consumer confidence. With economic releases looking increasingly mixed, the ML team seems challenged in support of their more optimistic view.

In any event, there most definitely seems to be a very subtle – yet discernible – to and fro taking place between Rosie and his former shop.

One of the biggest clouds on the economic horizon is the vast amount of debt U.S. households took on during the boom years. The Federal Reserve puts total household debt, including mortgage debt, at about $13.7 trillion, or 125% of annual after-tax income, a burden that many economists believe will take several years to pare down to what they see as a more sustainable level of 100%. During that "deleveraging" process, the logic goes, U.S. consumers -- whose spending makes up more than two-thirds of the U.S. economy and about one-fifth of the global economy -- won't be able to play a leading role in any recovery.

The gloomy forecasts, though, miss an important point: Debts have value only to the extent that they are being paid, and a rapidly rising number of U.S. households aren't doing so. Those defaults are leading to losses at banks, a wave of foreclosures, trouble for neighborhoods and strife for families. But they are also providing an immediate, albeit radical, form of debt relief.

"It's not ideal, because it carries other costs," said Karen Dynan, a consumer-finance specialist at the liberal Brookings Institution think tank who recently served as a senior adviser to the Federal Reserve. But it is "going to help get household balance sheets back to the right place."

If one accounts for defaults, U.S. households' debt burden is shrinking a lot faster than the official data suggest. First American CoreLogic, which tracks the performance of mortgage loans, estimates that some 9.3% of the nation's 52.4 million mortgage holders were 60 or more days behind on their payments as of July. That represents relief on about $1.2 trillion in loans. The official data miss most of that, because the Fed doesn't erase debts until banks have foreclosed, sold the homes and taken the loans off their books, a process that can drag out for more than a year.

As a result, some economists are expecting a sharp improvement as widely watched indicators of consumers' finances catch up to reality. Joseph Carson, director of global economic research at AllianceBernstein, expects the share of households' after-tax income that goes to pay loans, rent and other financial obligations to fall to 16.3% by the middle of next year, well below the average for the 20-year period leading up to the housing boom. As of June, it stood at 18.1%.

Home prices in 20 U.S. cities rose in August for a third consecutive month, bolstering the case that an economic recovery is at hand.

The S&P/Case-Shiller home-price index climbed 1 percent from the prior month on a seasonally adjusted basis after a 1.2 percent increase in July, the group said today in New York. From a year earlier, the gauge was down 11.3 percent, less than forecast.

Rising home sales, due in part to government programs including the first-time buyer credit and efforts to lower borrowing costs, have helped stem the slump in property values that precipitated the worst recession since the 1930s. Sustained gains in household spending, the biggest part of the economy, may be harder to come by as joblessness mounts.

The Chicago Fed Midwest Manufacturing Index (CFMMI) increased 1.0% in September, to a seasonally adjusted level of 82.3 (2002 = 100). Revised data show the index rose 1.6% in August, to 81.6.

Click for a larger image.

Click for a larger image.

Texas factory activity declined in October, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index—a key indicator of current manufacturing activity—edged further into negative territory, suggesting output in October contracted after remaining stable in September.

It is unfortunate that it took a force the size of the U.S. government to shake up the board and management at GM. In effect, the government has become the world's biggest activist investor, making the same kinds of demands that any activist or creditor should rightfully make in return for its investment.

Shaking up managements and boards is a no-brainer at underperforming companies for activist hedge funds and private equity firms, including Quadrangle Group, which Rattner co-founded. Why should investors tolerate poor performance? Why should taxpayers?

I have shaken up boards and managements at many companies in which I have invested, including Blockbuster, ImClone, Stratosphere, Philips Services, Federal-Mogul and many others. Generally, but not always, the net result has been very positive for the company and the shareholders. It is important to get new blood, new strategies and new ideas into underperforming companies.

As the saying goes, 'if you do the same thing all the time, you get the same result.' This applies to many managers. Too many are one-trick ponies. America is losing its economic hegemony because of it.

But most importantly, it is up to shareholders to step up to the plate and demand changes at their companies. For too long and for a variety of reasons, shareholders have been complicit in allowing management excesses and incompetence by not taking a stand.

"Shareholders have reelected these directors, have approved these pay plans and have been enablers for the addictive behavior of the corporate community," said Nell Minow, editor and co-founder of the Corporate Library in a recent BusinessWeek interview.

Let's hope the global economic meltdown causes shareholders to demand more changes on the part of their companies -- and not leave it to the government.

"Companies across the economy are holding off on hiring even as the profit outlook improves, amid economic uncertainty and their own success at raising productivity in rough waters.... Hiring always lags behind in economic recoveries, but the outlook this time is worse, many economists say. Most forecasters now expect a prolonged period of high unemployment ...."He next notes that Job opportunities are scarce, relying on the Job Opportunities and Labor Turnover Survey, a/k/a "JOLTS", to the effect that

"At the end of August there were estimated to be fewer than 2.4 million job openings, equal to only 1.8 percent of the total filled and unfilled positions—a new record low."Additionally, Job losses have been disproportionately concentrated in small businesses :

"[B]usinesses with fewer than 50 employees account for about one third of net employment gains in expansions. They have accounted for about 45 percent of job losses since the beginning of this recession. Given that these are the types of businesses most likely to be dependent on bank lending—and given that bank lending does not appear poised for a rapid return to being robust—the prognosis for an employment recovery in these businesses is a question mark."Next, he notes the large number of people who are Involuntarily working part-time , which,

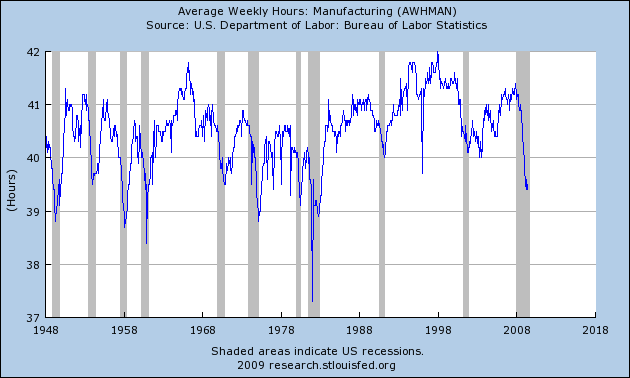

"at 8.8 million, [is] well above the level of past contractions in both absolute and relative terms..... One potential implication of this fact is that firms probably have the capacity to expand production without hiring new workers (or increasing worker productivity). All these firms have to do is give more hours to existing workers...."Finally,

"the percentage of employee separations labeled permanent is at a recorded high..... [T]hose who have been permanently separated from your previous employer, who has no expectation of hiring [them] back..... The last category is the dominant reason for unemployment at this time. That might not seem surprising, but it actually is. Never, in the six recessions preceding the latest one, did permanent separations account for more than 45 percent of the unemployed. The current percentage stands at 56 percent as of September and appears to be still climbing."Concludes Altig:

"none of this is proof positive that we are in for a "jobless recovery," but, to me, the odds appear to be increasing."While I certainly respect the credentials and the perspicacious analysis of Mr. Altig, as he says, it isn't proof positive, and there are some limitations in his argument that cause me to find it less than convincing. In the first place, two of the data series he relies on are less than 20 years old. The small business hiring data only goes back to 1992, and the JOLTS survey only goes back a decade! Saying that one of these series is "at a record" is not the same thing the same statement made for a data series with 50 or 100 years of data behind it. Additionally, the JOLTS data didn't turn more positive until summer 2003 after the last recession, clearly showing that it is a lagging indicator. Most likely the jobs turn will have already happened by the time it shows up in the JOLTS data.

| Month | Mfg # lost | Services # lost |

|---|---|---|

| 1979-82* | 3.6M | 0.3M |

| 1990-91 | 2.1M | 0.4M |

| 2001-03 | 3.0M | 0.5M |

| 12/2007-8/2008 | 0.6M | 0.4M |

| 8/2008-9/2009 | 2.9M | 3.2M ! |

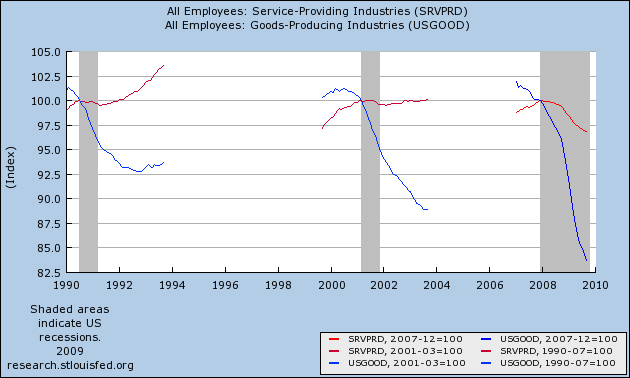

In a Keynesian recession, you are temporarily laid off because of excess inventories and deficient aggregate demand. You wait to be recalled by your firm. This was true of recessions from the end of the second World War through the 1980 recession. Even the 1975 recession, which was a "supply shock" (higher oil prices, requiring some permanent readjustments), had a relatively low share of permanent job losses.While Kling meant to support Altig's point, I think Kling's argument actually undercuts that for a "jobless recovery," precisely because the overwhelming share of job losses in the 1991 and 2001 recessions were in manufacturing -- which, due to productivity enhancements and China, never came back. This time around, with over half of the job losses in services, workers do not need to learn a whole new set of skills in order to return to the labor force. What is needed is an increase in real consumer spending, which -- as I have shown in this graph before, and repeat here

In a Recalculation, you permanently lose your job and you have to find something else. The Recalculation model increasingly holds as we move away from an economy dominated by manufacturing. Even though the 1990 and 2000 recessions were relatively mild, a large share of the job losses were permanent.