The measures chosen to counter the onset of a "Great Depression 2" are having the desired affect of increasing economic activity, and they have saved - and finally, actually created - jobs in the economy. But those same measures are increasing the gulf between the rich and the rest of us, and between Too Big To Fail big business and everybody else.

That truth hits home in several news releases about the different-as-night-and-day outlooks between big businesses and small businesses in the last few weeks. Big Businesses are experiencing big profits, and may be having their most profitable year EVER Yes you read that right. Meanwhile small businesses are as pessimistic as they were in the depths of the cliff-diving a year ago. It turns out that, surprise surprise, where you aim your firehose of new money has a profound effect on which parts of the economy benefit mightily, and those that are left to wither on the vine.

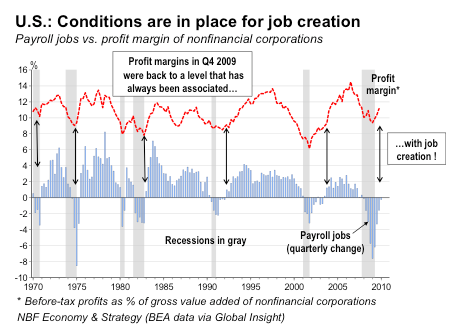

This entry has its genesis in a jarring graph I saw a couple of weeks ago in the National Bank Financial Group newsletter (pdf). It shows that the rate of corporate profits can be a "leading indicator" for job growth:

It makes sense. Once businesses start making enough money, they can spend some of it on hiring new employees to expand their business. But the idea that business are already seeing robust profits, this quickly after the worst Recession in decades makes the populist in me seethe.

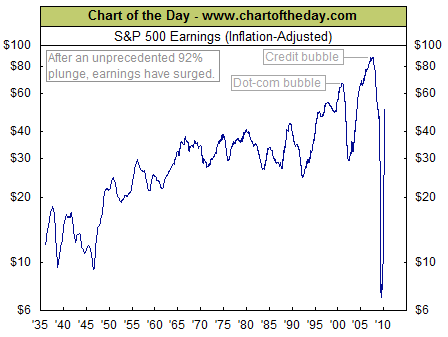

It isn't just the *rate* of profits. The *amount* of profits made by the companies included in the S&P 500 -- which account for about 2/3 of all economic activity in this country -- have been showing a V-shaped recovery in spades:

and that graph is a few months old.

and that graph is a few months old.Indeed, Barrons, the weekly financial newsmagazine reported the week before last that analysts expect that by the end of the third quarter -- less than 6 months from now -- the S&P 500 will show their most profitable year *in hsitory* -- bigger than 2000, bigger than 2006, bigger than 2007! Here's a sample of the outlook they cite:

Much of the rally of the past year has been in anticipation of a profit recovery. And now that recovery is actually coming in a bit better than bulls expected, which is why they are able to elbow bears so effectively. ISI Group now figures that corporate profits will clock in at +38.8% for the first quarter (year over year) of 2010, then +42.4% in the second quarter, +36.8% in the third quarter and then +30% in the fourth quarter (against harder comparisons). That would put profits in 2010 up a record 36.1% overall.

If America's 500 largest corporations are on their way to showing record profits, the mom-and-pop small businesses that are reported on by the National Federation of Independent Businesses are still mired in depression. On Tuesday the NFIB reported that its:

Business Index of Small Business Optimism lost 1.2 points in March, falling to 86.8. The persistence of index readings below 90 is unprecedented in survey history.

“The March reading is very low and headed in the wrong direction,” said Bill Dunkelberg, NFIB chief economist. “Something isn’t sitting well with small business owners. Poor sales and uncertainty continue to overwhelm any other good news about the economy.”

There is no optimism, no rising profits, and no capital investment going on at these small businesses. The only silver lining is that they are no longer shedding workers (a fact confirmed by the Dan Froomkin:

[Robert] Rubin [, ...] who's been almost exactly 180 degrees wrong on the major economic issues of his time thinking these days [ ], in an essay published by Newsweek late last year, [ ] worried about too much spending on job-creation, opposed forcing the riskiest derivative contracts onto public exchanges, resisted an accounting reform that would require financial institutions to assess their assets based on actual market prices rather than just making things up, and warned against what he calls impractical proposals to break up "too big to fail" banks. His most pressing concern was the federal deficit. All in all: A decidedly Wall Street rather than Main Street agenda.

Why is this happening? It has to do with the theory of the "first receiver" of new money:

Money creation [warning:pdf] might be of gain for the receiver of the new money, who receives it without a productive effort. The newly created money spreads through the economy as the first receiver spends it on particular goods, bidding up prices and, thus, raising the revenue of the sellers of those goods. But it is at the expense of those who are the ones that are the last to receive part of the new money, while at the same time have to pay higher prices. And then there is the risk of bank failures, a risk everybody will be affected by. Hence, we see that the bankers, the merchants and the government are the first to benefit by the creation of fiduciary media. But this also means that it is at the expense of other parts of the population. And at a crisis, everybody is likely to lose.

....

A real world example of how this problem of first/early receivers of easy money and credit vs. late/non-receivers played out in the housing bubble was well-described in 2004 by Frank Shostak:

As a result of loose monetary policy, which aims to "protect" the financial system, financial institutions always receive the new money first. Obviously this gives rise to an expansion of activities of the earlier receivers of money. An early receiver of money can afford, so to speak, to become more of a risk taker and undertake various risky activities.

In reality however, the new money leads to an exchange of nothing for something. It leads to the enrichment of the earlier receivers and to the impoverishment of the late or nonreceivers of the new money. Money and credit out of thin air leads to a redistribution of real wealth.

(N.B.: The last two quotes come from people identified as "Austrian economists." While this school has lots of problems, it described what happened in the last 5 years or so extremely well) Begging your pardon, let me quote from myself a year ago when I wrote that Why the Wall Street Bailout will Harm average Americans -- even if it works!:

The gifting of Wall Street and its counterparties directly with $Trillions creates the exact same first/early receiver vs. late/non-receiver problem as with the gifting of fog-the-mirror credit to purchase houses: this is real money, and it is going into concentrated hands. Those parties can -- indeed are intended to -- use that cash in an effort to prop up the value of assets they hold. That money will only slowly spread into the general economy (remember how we were told in September [2008] that we needed to rescue Wall Street so that they would continue to lend to Main Street businesses?), by way of certain business, and lastly of all, if at all, to the average American household -- who will be faced with even more inflated values for assets compared with their households' purchasing power.

In summary and conclusion, even if the various Wall Street bailouts succeed, they will continue and amplify the trend that has been in place for 30 years: creating yet a wider gulf between the wealthy and the financially connected, and the average American and his/her family, rewarding the former while punishing the latter, who already during this last business cycle, for the first time since the Great Depression, saw their real wealth and income decline.

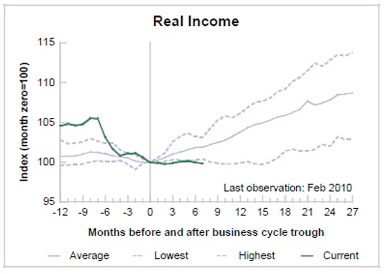

This increasing gulf between the Ultra-Haves and Everybody Else is bad social policy. And it is the premier reason why the Gilded Recovery is, as I wrote a month ago, also a "Bifurcated Recovery" where GDP, Industrial Production, Manufacturing and Exports are on having V-shaped increases, while job creation has only just started and looks like it will take years to recover. And there's more: As James Suroweicki points out in a New Yorker article, while depending on how you count, only 10% or 17% of Americans are unemployed, the other 83% to 90% do have jobs. Thus more than just employment or unemployment, it is real income that matters to Amercians because *all* wage and salary earners feel the direct effects of the growth - or not - of real income. And real income is bouncing along the bottom, having turned up just barely from its absolute bottom last year:

A society whose Gini coefficient of wealth is high and rising is not a society on a good or healthy path.