It's that time of the week. Don't think about the market or the economy until Monday. Until then ....

Investment is non-residential structures increased a bit last quarter

Investment is non-residential structures increased a bit last quarter

Services make up the largest percentage of PCE expenditures, comprising about 65% of PCEs. They have expanded for the last three quarters at an uneven pace.

Services make up the largest percentage of PCE expenditures, comprising about 65% of PCEs. They have expanded for the last three quarters at an uneven pace. Non-durable purchases also increased last quarter, but at the slowest pace in the last four quarters.

Non-durable purchases also increased last quarter, but at the slowest pace in the last four quarters.

The increase in real GDP in the second quarter primarily reflected positive contributions from nonresidential fixed investment, exports, personal consumption expenditures, private inventory investment, federal government spending, and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The deceleration in real GDP in the second quarter primarily reflected an acceleration in import and a deceleration in private inventory investment that were partly offset by an upturn in residential fixed investment, an acceleration in nonresidential fixed investment, an upturn in state and local government spending, and an acceleration in federal government spending.

Labor market conditions improved gradually in several Districts. New York, Chicago, Minneapolis, Richmond, and Atlanta all reported that labor markets improved, albeit modestly in some cases, while Boston and Dallas reported that employment was steady. Philadelphia, Atlanta, Richmond, Chicago, and Minneapolis reported that temporary employment experienced increased demand. Contacts in the Philadelphia, Atlanta, Dallas, and San Francisco Districts said that they continued to rely on temporary staff over permanent hires. Cleveland, Richmond, and Chicago saw hiring in the manufacturing sector. Cleveland also reported some new job openings in the healthcare industry. Boston and Cleveland noted that firms in some services industries were hiring mostly for replacement. Dallas reported that firms in the energy industry experienced significant regional layoffs as a result of the deepwater drilling moratorium. San Francisco noted continued high levels of unemployment and limited hiring.

Reports on retail sales during the early summer months were generally positive, although in most Districts the increases were modest. Retail sales in the New York, Philadelphia, Minneapolis, and Kansas City Districts were higher than year-earlier sales, and Dallas reported solid gains. But sales in the Boston District were mixed compared with the previous year. Recent sales increased slightly in the Cleveland, Atlanta, Chicago, and San Francisco Districts; sales in the Richmond District weakened; and sales in the Kansas City District were flat compared with the previous report. Several Districts cited apparel, food, and other necessities as recent strong sellers, while big-ticket items were weak sellers. Contacts reported satisfactory inventory levels in the New York District, mixed inventory levels in the Boston District, and low or declining inventory levels in the Richmond, Atlanta, and Chicago Districts. The outlook for sales was mixed: Retailers in the Philadelphia, Cleveland, Kansas City, and Dallas Districts reported that they expect modest positive sales growth in the upcoming months; contacts in the Cleveland, Atlanta, and Chicago Districts reported a less optimistic outlook going forward than in the previous report; and retailers in the Boston District reported a cautious outlook.The Districts that reported on auto sales during the early summer months generally noted a decrease in recent sales. Since the previous report, auto sales in the New York, Philadelphia, Cleveland, Richmond, Chicago, and San Francisco Districts declined, while auto sales in the Kansas City District increased and were unchanged in the Dallas District. Compared with last year, auto sales in the Atlanta and St. Louis Districts were higher. New York, Philadelphia, Cleveland, Chicago, Kansas City, and Dallas all reported that inventory levels were low or declining. Auto dealers anticipate little change in sales for the rest of 2010 in the Philadelphia District and expect sales to increase slowly in the Dallas District. Contacts in the Kansas City District expect continued strong demand, while those in the Cleveland District do not anticipate strong growth in the coming months.

Economic activity has continued to increase, on balance, since the previous survey, although the Cleveland and Kansas City Districts reported that the level of economic activity generally held steady. Among those Districts reporting improvements in economic activity, a number of them noted that the increases were modest, and two Districts, Atlanta and Chicago, said that the pace of economic activity had slowed recently.Manufacturing activity continued to expand in most Districts, although several Districts reported that activity had slowed or leveled off during the reporting period. Districts also noted improved conditions in the services sector. The five Districts reporting on transportation noted increased activity. Tourism activity also increased across the Districts, although the Atlanta District noted concerns about decreased leisure travel to the Gulf Coast. Retail sales reports generally indicated a continued rise in spending, and several Districts noted that necessities continued to be strong sellers, while big-ticket items moved more slowly. However, most Districts that reported on auto sales noted declines in recent weeks. Activity in residential real estate markets was sluggish in most Districts after the expiration of the April 30 deadline for the homebuyer tax credit. Commercial real estate markets, especially construction, remained weak. Banking conditions varied across the Districts, with some Districts noting soft or decreased overall loan demand; credit standards remained tight in most reporting Districts. Recent rains had mixed effects on crop conditions, while activity in the natural resources sector increased. Overall labor market conditions improved modestly across the Districts, with several reports of temporary hiring. Consumer prices of goods and services held steady in most reporting Districts. Input prices also held largely steady, with only a few reports of cost increases. Wage pressures continued to be contained on the whole.

So, the general trend is for an increased, albeit at a slower pace than before. While there is growth, it is "modest" and several districts reports a slowing trend.

Let's take the report section by section and then add some information as appropriate.

Manufacturing activity in most Districts continued to move up since the last report, although the pace of activity slowed or activity leveled off in the New York, Cleveland, Kansas City, Chicago, Atlanta, and Richmond Districts. Automobile manufacturing was a bright spot for the Cleveland, Chicago, and St. Louis Districts. Automobile parts suppliers also experienced increased demand in both the Richmond and Chicago Districts. Fuel demand at refineries in the San Francisco District improved, while gasoline demand was steady in the Dallas District. Firms in the semiconductor manufacturing industry reported relatively strong sales or demand growth in both the Boston and San Francisco Districts. Firms in aircraft and parts manufacturing saw sales pick up in both the San Francisco and Dallas Districts. Manufacturing firms in the Boston, Philadelphia, Kansas City, and Dallas Districts were optimistic that demand would continue to improve in the following months. However, Cleveland's contacts expect demand growth to taper off, Philadelphia noted that the balance of positive over negative views had narrowed, and Atlanta reported fewer firms planning expansions in production. Richmond, Chicago, and Dallas reported that firms in construction-related manufacturing experienced weak demand; construction supplies sales were flat in Kansas City, and Minneapolis reported that a firm in the sector was increasing production. Steel production declined in both the Chicago and Cleveland Districts. Some manufacturers in the Atlanta and San Francisco Districts reported high excess production capacity. Capacity utilization was below pre-recession levels in Cleveland and edged lower among steel producers in Chicago.

Manufacturing was one of the first areas of the economy to turn around. However, we are now seeing a slowdown in some areas. Let's take a look at some of the data:

While the ISM index is still increasing, it has moved lower over the last few months. However, the reading is still above 50, indicating an expansion of the manufacturing sector.

The NY Empire state index dropped last month, but it is also still in an area of expansion.

The Philadelphia Fed's manufacturing survey also dropped last month, but is also still positive.

The Richmond Fed's manufacturing index also dropped last month (it's obscured by the 3-month line). However, like the other regional indexes, it is also still positive.

The Texas index is also just above 0, but still positive.

Overall industrial production and capacity utilization are still increasing. However, the IP number last month was weak and the capacity utilization moved sideways. But -- this is one month of data, not the general trend.

So, the latest data point of a slowdown in manufacturing. The regional indicators all moved lower. But this is one month of data and the indicators are still positive.

Services

Unfortunately, there aren't as many service indicators as manufacturing. Here is a chart of the ISM non-manufacturing index:

Last month it dropped after three months are more or less the same level. It could be topping out, but we don't know if it will stay at this level or move lower.

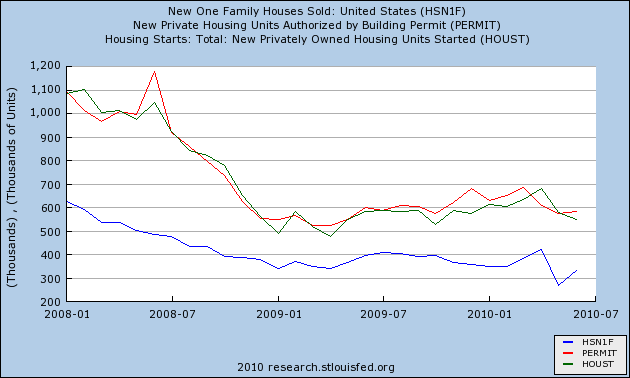

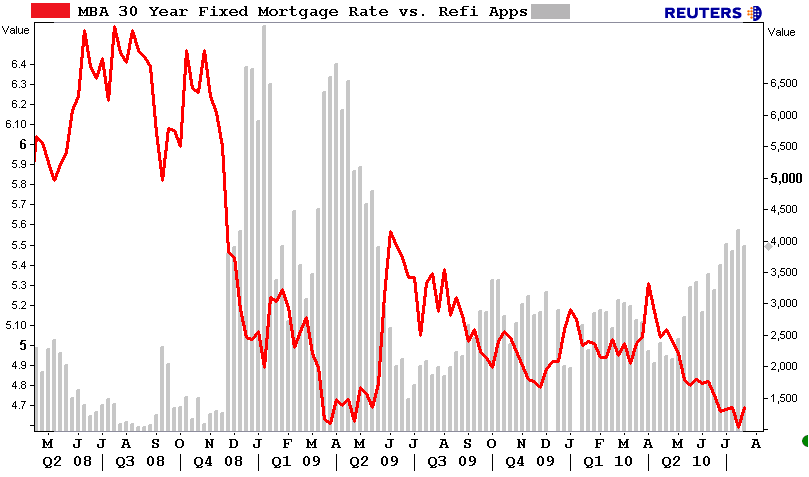

The seasonally adjusted Purchase Index increased 2.0 percent from one week earlier and is the highest Purchase Index observed in the survey since the end of June. The unadjusted Purchase Index increased 2.4 percent compared with the previous week and was 34.3 percent lower than the same week one year ago. The four week moving average is flat for the seasonally adjusted Purchase Index.It isn't just purchase mortgage applications. The Census Bureau reported on Monday that sales of single family homes rebounded strongly in June from an abysmal May (blue), and Permits also rose slightly from their May reading as well (red). Only starts, which frequently lag behind permits by one month, continued to decline in June (green):