Early last week January savings and spending were reported. I haven't updated those graphs in awhile, so this is a good opportunity to do so.

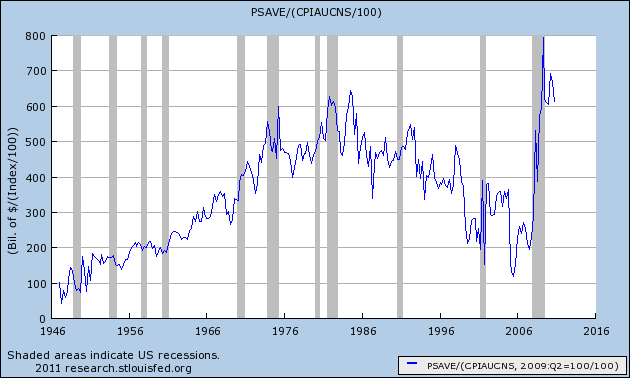

To begin with, on a real, inflation adjusted basis, Americans saved more money at the bottom of the Great Recession than at any time since World War 2:

As you can see, some of that savings has been spent to fuel the recovery so far, but most of the accumulated savings - as much as at the end of the 1980-82 recession - is still available.

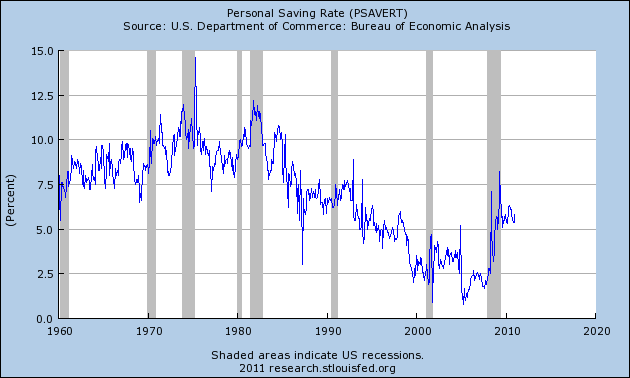

Amercians' relative newfound frugality can be seen in this update graph of the savings rate as well:

This has been trending sideways for over a year and a half, and from the longer term point of view, is a good thing.

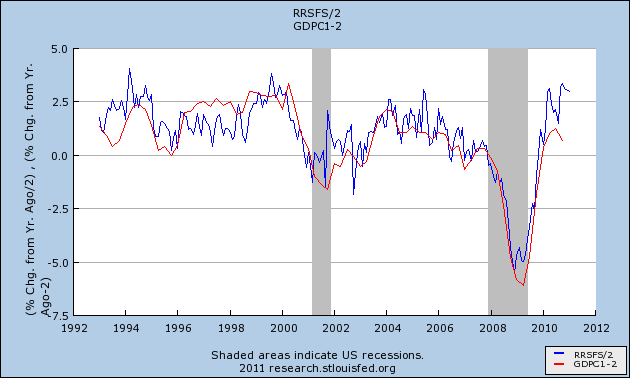

Yesterday I pointed out that job growth in 2010 tracked real GDP growth (red) more closely than real retail sales (blue). Which means that the two series have diverged more than usual, as you can see here:

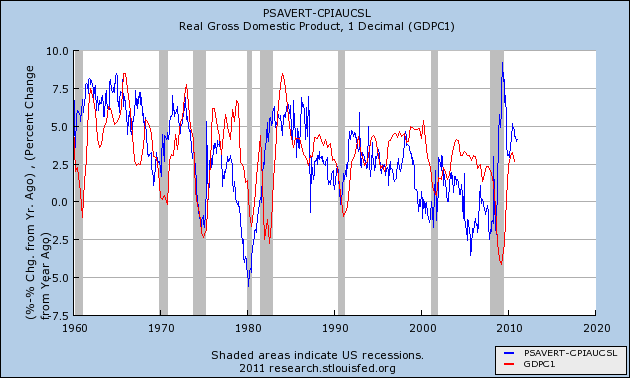

So, how will the divergeance get resolved? Back in August of last year I began keeping track of the real, inflation adjusted personal savings rate, and updated that view in November. Here is how the relationship between the real personal savings rate (blue) and real GDP (red) stands now:

As I said then, the reason for keeping track of the relationship is that as can be seen in the above graph, a substantial change in the real personal savings rate is mirrored by a similar substantial change in real GDP about 6 to 18 months later. Subtract 2% from that change in real GDP, and you have a reliable prediction of the change in jobs growth and the unemployment rate another 6-12 months after that. The logic of this isn't hard to follow: increased savings serve as the "tinder" that ignites subsequent spending. That spending leads to growth, and then that growth leads to the creation of jobs.

Thus an increase in savings is a "long leading indicator" for employment in a range of 18 to 30 months later. We are now about 21 months past that peak increase in savings, so this relationship predicts further increases in YoY job growth in 2011. As I pointed out back in November, "subsequent GDP increases are generally similar to the precursor real personal savings rate -- which has been above 5% for much of the last 18 months. Which means that an unemployment rate significantly under 9% by the end of 2011 is quite doable."

The dramatic drop in the unemployment rate in the last three months bears that out. Put another way, the high "real personal savings rate" argues that the divergence between real GDP and real retail sales will be resolved towards the higher indicator - which also suggests continued robust jobs growth.