Recently most important items of economic data -- housing permits, car sales, new jobless claims, payrolls, consumer confidence, etc. -- have all moved substantially in the right direction. But there is always a bearish case to be made, and the best one, it seems to me, focuses on the consumer.

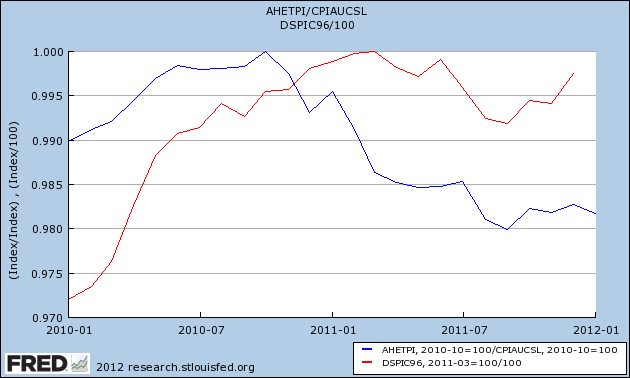

Here's a graph of real hourly wages (i.e., wages minus the CPI) (blue) and real disposable income (red) for the last year:

As you can see, real wages declined by about 2% since late 2010. Real disposable income also declined beginning last spring and so far has not made up all of the loss.

Primarily but not solely due to gasoline prices, consumers have had to dig into savings accumulated during the "great recession" to continue spending, causing a decline in both savings (blue) and the savings rate (red):

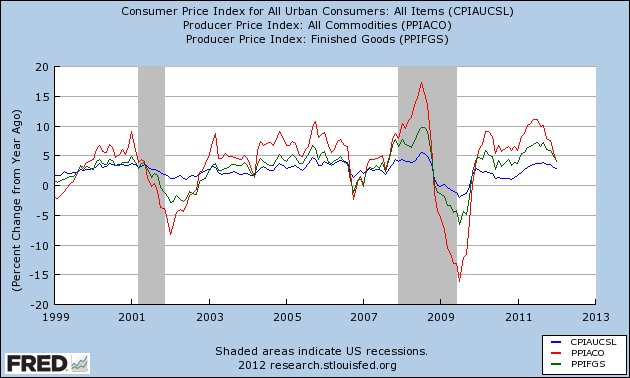

In the past, a spike in inflation has always led to economic weakness - shown in a decline in measures of inflation. Note that in 2001 and 2008, when commodity prices (red) and finished goods prices (green) declined to the same level as consumer prices (blue), we were about midway through the recession:

Even the two cases where commodity prices did not weaken significantly more than consumer prices (2003 and 2006) coincided with brief periods of especially weak GDP growth.

This is consistent with the fact that a number of long leading indicators -- Real M2, housing permits, and bond prices -- bottomed after a period of significant weakness about 12 months ago. Typically that weakness is most manifest in the consumer economy in about 1 year or so -- i.e., now.

In that regard it's worth noting that the most recent proprietary article on ECRI's site is entitled, "Can the US consumer keep spending?" Based on last Friday's round of interviews, obviously they think not.

Barring a reversal of fortune, ECRI is probably right about the US consumer. But note that none of the above graphs are predictive rather than explanatory. In fact real wages and real disposable income have rebounded slightly since autumn, and there is nothing inherent in any of the above graphs indicating that this rebound will not continue.