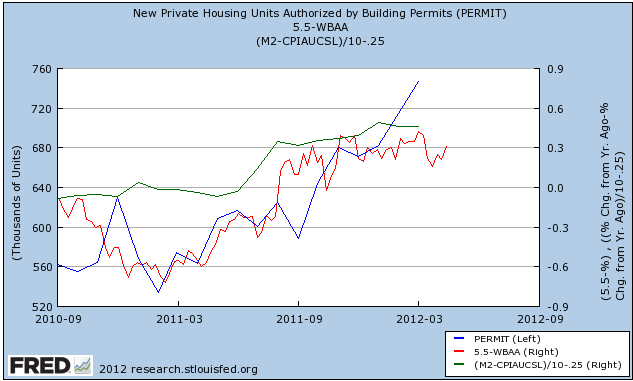

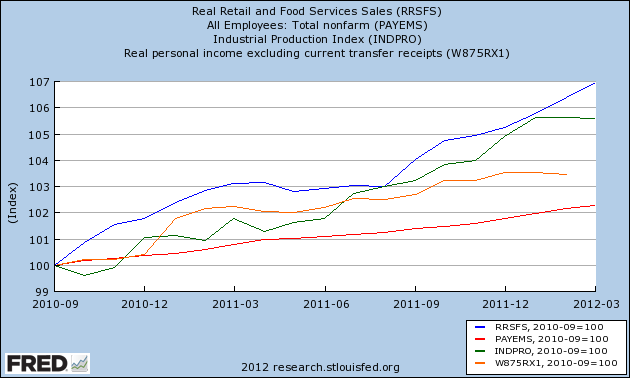

The monthly data releases this week included a continuing if small advance in the Leading Economic Indicators of +0.2. While the Conference Board's spokesman isn't all over the cable news networks promoting its views, it is important to note that this series, after declining slightly late last summer (forecasting weakness now), has consistently increased since then. Retail sales and real retails sales both came in strongly positive. So did housing permits, rising to a 3 1/2 year high and no longer "bouncing along the bottom." Housing starts, however, did decline significantly. Industrial production remained flat. Existing home sales showed slight weakness.

The high frequency weekly indicators this week give important evidence of two areas of the economy going through fundamental transitions. Of particular interest are the H8 FRB series of real estate loans and house price indexes, and also the very important coincident indicator of rail traffic, not only for what is happening, but why it is happening.

Let's start with the Housing reports :

The Mortgage Bankers' Association reported that the seasonally adjusted Purchase Index decreased -11.2% from the prior week, and was also off -13.9% YoY. Looking at the MBA's database, this may be a calendar quirk, as purchase mortgages declined strongly in the next week one year ago. The Refinance Index reversed course with a strong increase of +13.5% from the previous week. Because the MBA's index was substituted for the Federal Reserve Bank's weekly H8 report of real estate loans in ECRI's WLI, I've begun comparing the two. This week for the second third week in a row after 4 years of relentless decline, real estate loans held at commercial banks were up, +1.0% on a YoY basis. On a seasonally adjusted basis, these bottomed in September and are now up +1.7%.

YoY weekly median asking house prices from 54 metropolitan areas at Housing Tracker were up +3.1% from a year ago. YoY asking prices have been positive now for close to 5 months. This week Realtor.com reported that asking prices for their entire database were up 5.6% YoY in March. Further, the NAR reported that a 2.5% YoY increase in median home sale prices for March. At this point virtually the only house price indexes that haven't turned positive YoY are the repeat sales indexes like Case-Shiller.

Now let's turn to the effects of the Oil choke collar:

Gasoline prices fell slightly for the first time in months, to $3.92. Oil, however, rose slightly to $104.02. Both of these remain above the point where they can be expected to exert a constricting influence on the economy. Gasoline usage, at 8775 M gallons vs. 9062 M a year ago, was off -3.2%. The 4 week moving average is off -2.8%. These are among the best YoY comparisons in months, but on the other hand one year ago gasoline usage was beginning its big decline.

The American Association of Railroads reported a -2.9% decline in traffic YoY, or -15,300 cars. Ex-coal, overall traffic was up by 8,400 cars, or +1.6% YoY. Intermodal traffic was up 3700 carloads, or +1.6%, but other carloads decreased -19,000, or -6.4% YoY. Railfax's graph of YoY traffic continued to show that rail hauling of cyclically sensitive materials remains in strong improvement. Beyond coal, the other groups suffering declines have to do with corn-related agricultural products, and this in turn has everything to do with American consumer's single-minded quest for energy efficiency. CSX was the first railroad to report Q1 earnings, and as reported by ABC News:

CSX said the market for utility coal is likely to be even weaker in the second quarter, but the Jacksonville, Fla., company said it's on track to top 2011 earnings this year. Shipments of agricultural products dipped 1 percent as demand for ethanol, which is made from corn, dropped because motorists have been buying less gasoline. Ethanol is added to much of the gasoline used in the U.S.Employment related indicators were mixed:

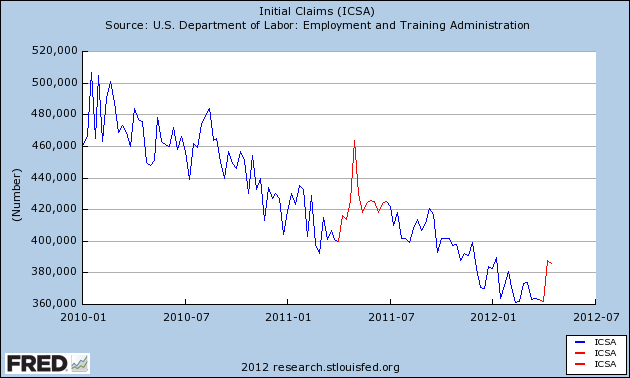

The Department of Labor reported that Initial jobless claims rose another 2,000 to 382,000 last week*, the highest report since January, thus continuing to mirror the big increase in April one year ago. The four week average also rose by 6250 to 374,750. (*In these summaries I always compare the raw number from the week prior to the raw number this week, avoiding the w/w distortion that takes place when we know that late reports will increase the prior week's number usually by 2000 to 6000).

The Daily Treasury Statement showed that for the first 14 days of April, $103.6 B was collected vs. $104.4 B a year ago, the second week in a row showing an absolute decline. In the last 20 reporting days, however (a more valid measure), $138.2 B was collected vs. $132.3 B a year ago, an increase of $5.9 B, or +4.5%.

The American Staffing Association Index rose held steady at 90. It remains close to its pre-recession readings of 2007.

Sales remained a positive.

The ICSC reported that same store sales for the week ending April 14 fell -1.0% w/w, but rose +3.2% YoY. Johnson Redbook reported a 3.0% YoY gain. Shoppertrak reported a -1.0% YoY loss, probably having everything to do with the timing of Easter this year vs. last year. The 14 day average of Gallup daily consumer spending remained favorable at $74 vs. $68 in the equivalent period last year.

Money supply was mixed on a weekly and monthly basis: M1 fell -0.2% last week, but was up +1.0% month over month. Its YoY level increased to +18.1%, so Real M1 is up 15.5%. YoY. M2 fell -0..1% for the week, but was up +0.4% month over month. Its YoY advance rose slightly to +9.9%, so Real M2 was up 7.3%. Real money supply indicators continue slightly less strongly positive on a YoY basis.

Bond prices rose and credit spreads widened again: Weekly BAA commercial bond rates fell -.10% t0 5.19%. Yields on 10 year treasury bonds fell +.17% to 2.04%. The credit spread between the two, which had a 52 week maximum difference of 3.34% in October, rose again to 3.15%, suggesting a weakening in economic conditions.

Turning now to high frequency indicators for the global economy:

The TED spread rose .02 to 0.400. This index remains slightly below its 2010 peak, generally steady for the last 7 weeks, and has declined from its 3 year peak of 3 months ago. The one month LIBOR remained at 0.240. It is well below its 12 month peak set 3 months ago, remains below its 2010 peak, and has returned to its typical background reading of the last 3 years.

The Baltic Dry Index at 1067 was up 95 from 928 one week ago, and up 397 from its 52 week low, although still well off its October 52 week high of 2173. The Harpex Shipping Index rose 15 to 410 in the last week, and is up 35 from its February low of 375.

Finally, the JoC ECRI industrial commodities index fell from 123.74 to 122.31. It has resumed its fade, at a pace about equal to exactly one year ago. This indicator appears to have more value as a measure of the global economy as a whole than the US economy.

This week the monthly and weekly indicators together showed an important transition in the real estate market. Housing permits are THE leading indicator for that sector, and they have broken out of a 3 year bottom to the upside, now more than 200,000 units on an annual basis above their 2009 lows. The rapid turnaround in real estate loans by banks to the upside is also a leading indicator, confirming the story told by permits. That more and more price index series have turned up lends even more credence to the (relative) firming of the real estate market.

Secondly, consumers' laser-like focus on saving on energy costs is now affecting mining, rails and utilities in addition to gasoline usage in vehicles. The decline in those indicators is a negative for the economy, but I suspect it is more than offset by the efficiency gains and the cash freed up for other spending by energy consumers, as is evident in the continuing strength of retail sales.

Money supply was mixed on a weekly and monthly basis: M1 fell -0.2% last week, but was up +1.0% month over month. Its YoY level increased to +18.1%, so Real M1 is up 15.5%. YoY. M2 fell -0..1% for the week, but was up +0.4% month over month. Its YoY advance rose slightly to +9.9%, so Real M2 was up 7.3%. Real money supply indicators continue slightly less strongly positive on a YoY basis.

Bond prices rose and credit spreads widened again: Weekly BAA commercial bond rates fell -.10% t0 5.19%. Yields on 10 year treasury bonds fell +.17% to 2.04%. The credit spread between the two, which had a 52 week maximum difference of 3.34% in October, rose again to 3.15%, suggesting a weakening in economic conditions.

Turning now to high frequency indicators for the global economy:

The TED spread rose .02 to 0.400. This index remains slightly below its 2010 peak, generally steady for the last 7 weeks, and has declined from its 3 year peak of 3 months ago. The one month LIBOR remained at 0.240. It is well below its 12 month peak set 3 months ago, remains below its 2010 peak, and has returned to its typical background reading of the last 3 years.

The Baltic Dry Index at 1067 was up 95 from 928 one week ago, and up 397 from its 52 week low, although still well off its October 52 week high of 2173. The Harpex Shipping Index rose 15 to 410 in the last week, and is up 35 from its February low of 375.

Finally, the JoC ECRI industrial commodities index fell from 123.74 to 122.31. It has resumed its fade, at a pace about equal to exactly one year ago. This indicator appears to have more value as a measure of the global economy as a whole than the US economy.

This week the monthly and weekly indicators together showed an important transition in the real estate market. Housing permits are THE leading indicator for that sector, and they have broken out of a 3 year bottom to the upside, now more than 200,000 units on an annual basis above their 2009 lows. The rapid turnaround in real estate loans by banks to the upside is also a leading indicator, confirming the story told by permits. That more and more price index series have turned up lends even more credence to the (relative) firming of the real estate market.

Secondly, consumers' laser-like focus on saving on energy costs is now affecting mining, rails and utilities in addition to gasoline usage in vehicles. The decline in those indicators is a negative for the economy, but I suspect it is more than offset by the efficiency gains and the cash freed up for other spending by energy consumers, as is evident in the continuing strength of retail sales.

{kind=link}